While few people enjoy taking risks, they’re a normal part of investing and some risk actually serves a valuable purpose. If investors didn’t accept some risk, they wouldn’t have the potential to achieve higher returns. However, it’s important to ensure you’re not taking on unnecessary risk. The goal is to determine what level of risk you’re comfortable accepting and then balance it with the required risk necessary to achieve your long-term goals.

What is risk in the investment world?

Risk in the investment world is usually associated with market volatility. A commonly used phrase is, “Risk and return go hand in hand,” meaning the higher the return potential, the more volatility you must be willing to accept. Markets never move in a straight line — they experience ups and downs. Although the stock market has averaged over 11% annual return since 1977, it has only returned 5% to 15% 17 times, and only 9 times has it returned between 10% and 15% in a single year. The market has had more than twice as many up years (35) as down years (13), serving as a reward to long-term investors who can handle shorter-term volatility.

Range of Returns in the Toronto Stock Exchange (TSX)

1977 - 2024

| Total Returns | # of Years | % of Time |

|---|---|---|

| Greater than 30% | 6 | 13% |

| Between 15% and 30% | 12 | 25% |

| Between 5% and 15% | 17 | 35% |

| Between -5% and 5% | 4 | 8% |

| Between -15% and -5% | 8 | 17% |

| Between -30% and -15% | 0 | 0% |

| Worse than -30% | 1 | 2% |

Source: Morningstar Direct, S&P/TSX Composite Index, Total Returns. Past performance does not guarantee future results.

Risk is more than just volatility

Overall, individuals face many types of investment risk, such as interest rate risk, credit risk, economic risk and currency risk. Investors, meanwhile, often define risk as the potential for loss.

At its most basic level, risk refers to uncertainty and is much broader than volatility and the potential for (and size of) losses. Perhaps the biggest risk you may face is not reaching your financial goals. For example, a portfolio that is all in cash may have little, if any, volatility, but it also won’t provide any growth potential or inflation protection. For retirees, not keeping up with inflation, or not having the right withdrawal strategy, can lead to another major risk: the risk of outliving their money. Ultimately, the key is to determine what level of risk is appropriate to help you achieve your financial goals.

The balancing act

The next step is really a balancing act, as there sometimes can be a discrepancy between how much risk you are comfortable taking and how much you actually have to take to achieve your goals. This is where you may need to make some important decisions. Your financial advisor can help you build a portfolio that balances your risk tolerance, capacity for risk, and the risk you need to take to have a better chance of achieving your financial goals.

For example, suppose you want to retire at age 55, and you have a low risk tolerance. However, your financial advisor estimates that to accomplish this goal, you will need a higher return, resulting in a higher degree of portfolio volatility. In this case, you may have several choices, including working longer, saving more or accepting a higher degree of volatility. While this is a personal decision, by better understanding your goals, and the risks associated with achieving them, you can make a more informed decision.

Determining the right risk level

While risk may come in many forms, the process of determining what level of risk is appropriate covers three main areas:

- Risk tolerance - This refers to your willingness or comfort level with taking risk. Typically, you’ll be asked to complete a questionnaire that’s used to gauge how you might react to risk in different situations. Gauging risk tolerance and your potential behaviour is important because it’s unlikely you’ll reach your long-term goals if you abandon your strategy during inevitable short-term market declines.

- Risk capacity - While risk tolerance refers to your comfort with risk, risk capacity considers your ability to handle risk. Your investment time horizon is often one of the biggest factors in determining your risk capacity. For example, if you’re younger and preparing for retirement, you have a long time to make up for potential declines and could reasonably handle more volatility. However, if you’re retired, your ability to handle stock market declines is likely smaller. Other items, such as income needs, may influence your risk capacity. For example, retirees relying on their portfolios for a large portion of their income may not be able to handle as much volatility as those who have more discretionary income and are not as reliant on their portfolios for their retirement needs.

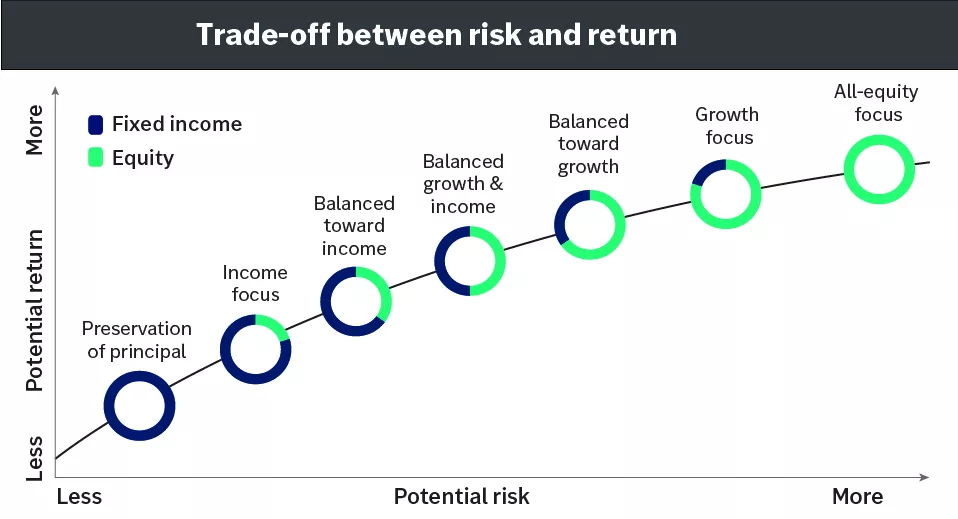

- Required risk - This refers to the level of risk we've estimated is required to achieve your investment goals. In the chart below, the higher the return needed to reach your goals, the more potential risk you’ll need to take to achieve them. As you discuss your goals with an Edward Jones financial advisor, you can determine which Portfolio Objective aligns with the return you need.

Trade-off between risk and return

This chart shows the greater the potential risk, the greater the potential return and vice versa. It uses a line that starts where the lowest risk and return meet and rises up to where the greatest risk and return meet. Portfolio objectives are indicated along the way that align with the combination of risk and return. reservation of principal is the portfolio objective that represents the lowest combination of risk and return; the second lowest combination is Income focus; the next lowest is Balanced toward income; the next up is Balanced growth & income; nearing the top where the highest risk and return meet is Growth focus; and the lastportfolio objective offering the greatest combination of risk and return is All-equity focus.

This chart shows the greater the potential risk, the greater the potential return and vice versa. It uses a line that starts where the lowest risk and return meet and rises up to where the greatest risk and return meet. Portfolio objectives are indicated along the way that align with the combination of risk and return. reservation of principal is the portfolio objective that represents the lowest combination of risk and return; the second lowest combination is Income focus; the next lowest is Balanced toward income; the next up is Balanced growth & income; nearing the top where the highest risk and return meet is Growth focus; and the lastportfolio objective offering the greatest combination of risk and return is All-equity focus.

Risk, your emotions and your success

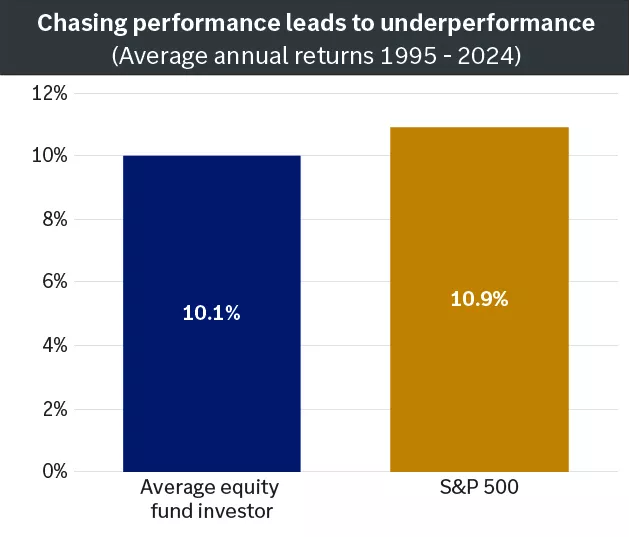

Typically, what prevents most investors from reaching their goals is not market volatility itself, but their reaction to this volatility. Investing based on emotions can often lead to one lasting emotion: disappointment. For example, the average investor’s equity investments performed worse than the S&P 500, as shown in the graph. It’s not because people owned the “wrong investments,” but because they chased performance, buying when stocks were up and then selling when they dropped in value.

Chasing performance leads to underperformance

This is a bar graph that shows the average equity investor realized a 6.81% average annual return for the past 30 years (from 1/1/1992 – 12/31/2022) compared to the S&P Index, which achieved a 9.65% average annual return during the period.

This is a bar graph that shows the average equity investor realized a 6.81% average annual return for the past 30 years (from 1/1/1992 – 12/31/2022) compared to the S&P Index, which achieved a 9.65% average annual return during the period.

Actions for investors

It’s important to discuss your goals and the amount of risk you’re willing to take to reach them with an Edward Jones financial advisor. You may need to make some difficult decisions. But, ultimately, these decisions may help you avoid the biggest risk you face: not reaching your financial goals.

Important information:

Past performance does not guarantee future results. The TSX is an unmanaged index and cannot be invested into directly. Diversification does not guarantee a profit or protect against loss.