Mid-2026: The second-half setup

What you need to know

- Markets displayed a broadening theme in June—a mix of international investments outperformed as tech cooled after a strong run, with bonds offering diversification benefits.

- Even with volatility from geopolitical risks and inflation pressures, disciplined investors have been rewarded with solid broad-based gains over the year.

- With a constructive backdrop unfolding, we have refined our guidance to help set up for the second half of 2026, emphasizing diversification to help capture broadening opportunities.

- Within our equity overweight, we now favour a mix of Canadian-, U.S.-, and emerging-market investments, with Canadian allocations tilted toward commodity- and infrastructure-linked sectors and U.S. allocations toward technology and cyclicals.

Portfolio tip

Broad diversification, backed by a disciplined rebalancing strategy, helps your portfolio more naturally benefit from leaders as markets rotate, reducing reliance on a narrow set of winners.

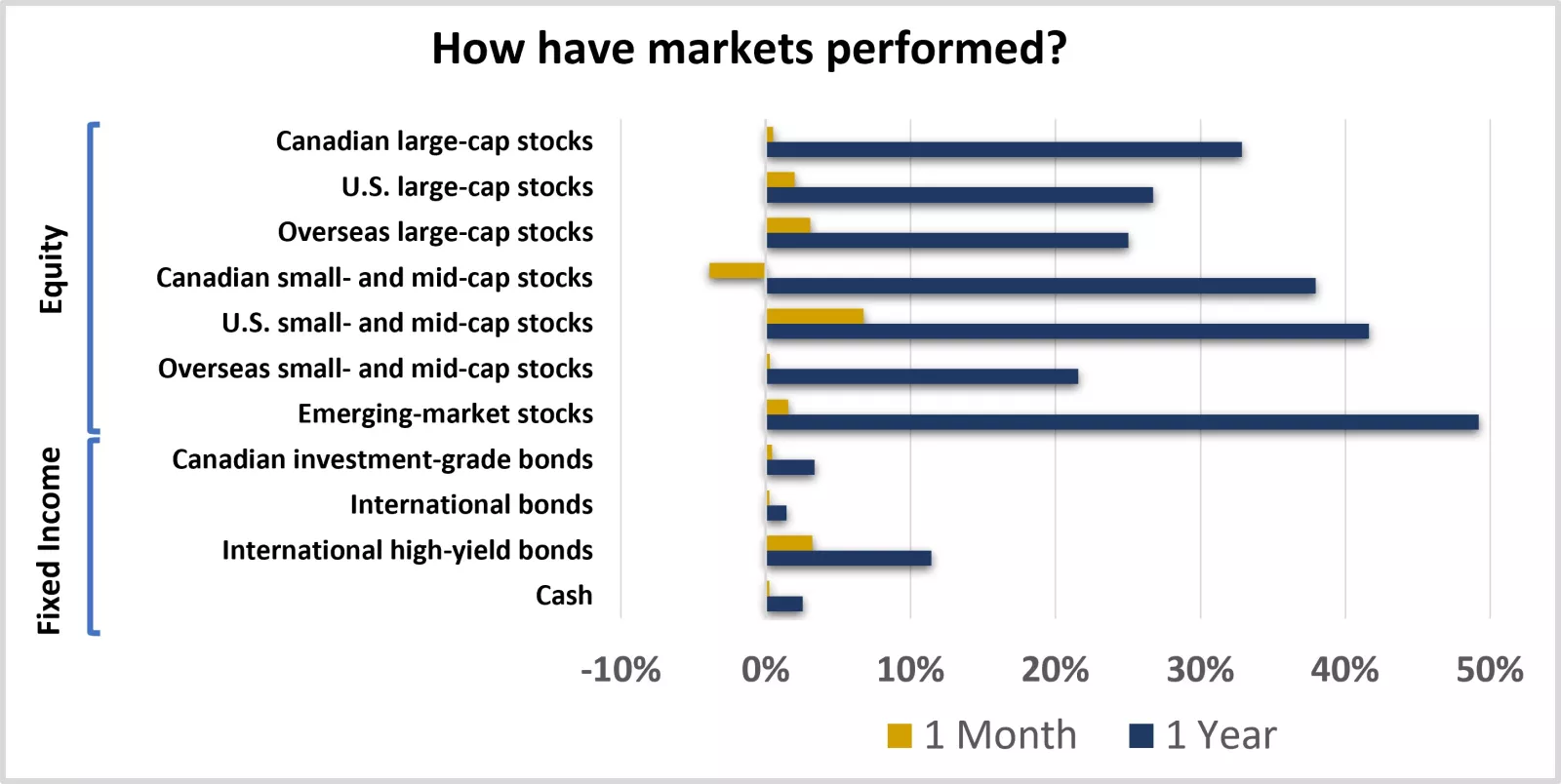

This chart shows the performance of equity and fixed-income markets over the previous month and year.

This chart shows the performance of equity and fixed-income markets over the previous month and year.

Where have we been?

Stock markets displayed a broadening theme in June, supporting the case for diversification. After heightened Middle East tensions and energy supply disruptions sparked a March pullback, rising expectations for a potential resolution in June sent oil prices back toward pre-conflict levels, helped ease inflation concerns and boosted economic optimism.

The resulting shift in market sentiment fueled a broadening of leadership beyond a narrow group of AI-driven stocks. Economically sensitive U.S. small- and mid-cap stocks were among the beneficiaries, extending their rally and claiming the month's top spot. A mix of cyclical and defensive sectors—financials, health care, consumer staples, industrials, and utilities—posted solid gains, as more growth-oriented sectors fell.

Despite strong earnings trends, the tech rally cooled in June as investors took profits and looked beyond a narrow set of large-cap technology stocks and key beneficiaries of the artificial intelligence buildout. As a result, U.S. large-cap and emerging-market stocks—each with roughly 40% exposure to the technology sector—were pressured yet managed to deliver gains on the improving sentiment more broadly. Energy and materials also relinquished leadership alongside declining commodity prices, weighing on Canadian stock markets.

Despite the year's volatility from geopolitics and inflation, disciplined investors were rewarded with broad-based gains. While June results were mixed and 2026 brought periodic market volatility, longer-term results display widespread gains across markets.

Backed by resilient economic growth and supportive corporate earnings trends, stocks were broadly higher over the last 12 months, outperforming bonds. Emerging markets, along with more cyclical Canadian and U.S. stocks, led with impressive gains. While overseas developed markets generally lagged, weighed down by their greater sensitivity to the conflict in the Middle East, they still delivered robust returns over the period.

Bonds continued to play an important role in portfolios. Even as central banks pivoted toward tightening to curb near-term inflation pressures, fixed income markets produced gains, helped by steady interest income, anchored long-term inflation expectations and de-escalating geopolitical tensions. More economically sensitive bonds outperformed amid a constructive economic environment, contained credit spreads and strong risk appetite.

What do we recommend going forward?

Emphasize diversification to capture expanding, rotating leadership. While elevated geopolitical tensions, near-term inflation pressures and evolving central bank policies may cause periodic volatility, our forecast for ongoing economic resilience, strong corporate profits and steady consumer trends suggest the backdrop for markets will remain supportive, offering broadening opportunities.

Broad diversification and a disciplined rebalancing strategy can help your portfolio more naturally benefit from leaders as markets rotate or the breadth of gains builds. As you conduct a mid-year portfolio review, consider not only reestablishing the stock-bond mix most appropriate for your financial goals, but also enhancing the resilience of your portfolio through strategic allocations across our seven recommended equity asset classes and four bond asset classes.

Emphasizing diversification in this way can help you stay prepared for what's next—rather than focusing on what has recently worked—while remaining aligned with your goals as markets shift.

Consider refining your portfolio's allocations to help set up for the second half of 2026 opportunistically. While we believe maintaining appropriately diversified allocations remains important, consider tilting your portfolio in these ways:

- Overweight equity investments, diversifying across Canadian-, U.S.-, and emerging-market opportunities. Specifically, we continue to favour U.S. large-cap and emerging-market stocks, partly due to their exposure to tech-driven growth and the benefits of global diversification. Overweighting U.S. stocks also helps to capture benefits from the relative strength of the U.S. economy. Strong momentum within emerging markets is also likely to be supported by the more cyclical nature of the asset class, especially as geopolitical tensions ease.

We recently reduced U.S. and overseas developed small- and mid-cap stocks to neutral and we remain underweight international large-cap stocks. Relative to other regions, we believe overseas markets now face slower growth prospects, given their greater sensitivity to Middle Eastern energy supply and near-term inflation pressures. We now prefer Canadian small- and mid-cap stocks, given their meaningful exposure to materials (roughly 35% of the asset class), industrials (20%) and energy (16%), three sectors we view favourably within our opportunistic Canadian equity sector guidance, described below.

At the same time, we raised international high-yield bonds to neutral to help enhance income potential for diversified portfolios amid a constructive economic backdrop, and we remain underweight investment-grade bonds

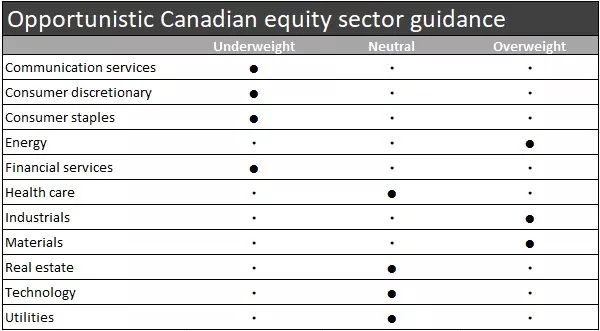

- Within Canadian stock allocations, overweight commodity- and infrastructure-linked sectors. The expected surge in power demand—in part due to data center buildout—growing support for expanding Canadian exports, and elevated commodity prices increase the attractiveness of the energy sector. Also consider overweighting industrials, which we expect to be supported by the earnings power within rail leaders, as well as by infrastructure demand backlogs across a variety of industries. And lastly, we expect materials to continue to be propelled by its gold and copper exposure amid elevated precious metal prices and valuations that appear relatively attractive.

We recently lowered financial services to underweight, alongside existing underweight positioning for communication services, consumer discretionary and consumer staples. While the financial sector has benefited from strong earnings recently, we believe risks related to high household debt and mortgage renewals could weigh on returns, particularly amid relatively elevated valuations.

- Within U.S. stock allocations, overweight tech-related and cyclical sectors. Given our expectation for the economic expansion to persist and for market leadership to potentially broaden, we continue to see opportunities in both technology and cyclical sectors relative to defensives. Consider overweighting the communication services and industrials sectors, offset by underweighting the consumer staples and utilities sectors.

We believe the industrials sector will continue to benefit from an ongoing manufacturing recovery. The communication services sector—which we recently raised to overweight—has lagged in the first half of the year and, as a result, valuations for the sector have declined and, in our view, do not reflect the exposure to secular growth among AI hyperscalers.

We recently lowered consumer discretionary to neutral. While steady labour market conditions and increased tax refunds have supported the sector, geopolitical tensions, rising inflation and high interest rates have caused pressure, suggesting a more balanced allocation at this time.

We’re here for you

With the second half of 2026 underway following a period of uneven market performance, now may be an opportune time for a portfolio review with your financial advisor. Our updated portfolio guidance is intended to help position you for the remainder of the year, reflecting our global outlook while staying aligned with your financial goals and comfort with risk—and may help guide your discussion.

If you don't have a financial advisor, we invite you to meet with an Edward Jones financial advisor for a mid-year portfolio check-up, exploring how you might update the positioning of your portfolio to set up for the year's second half.

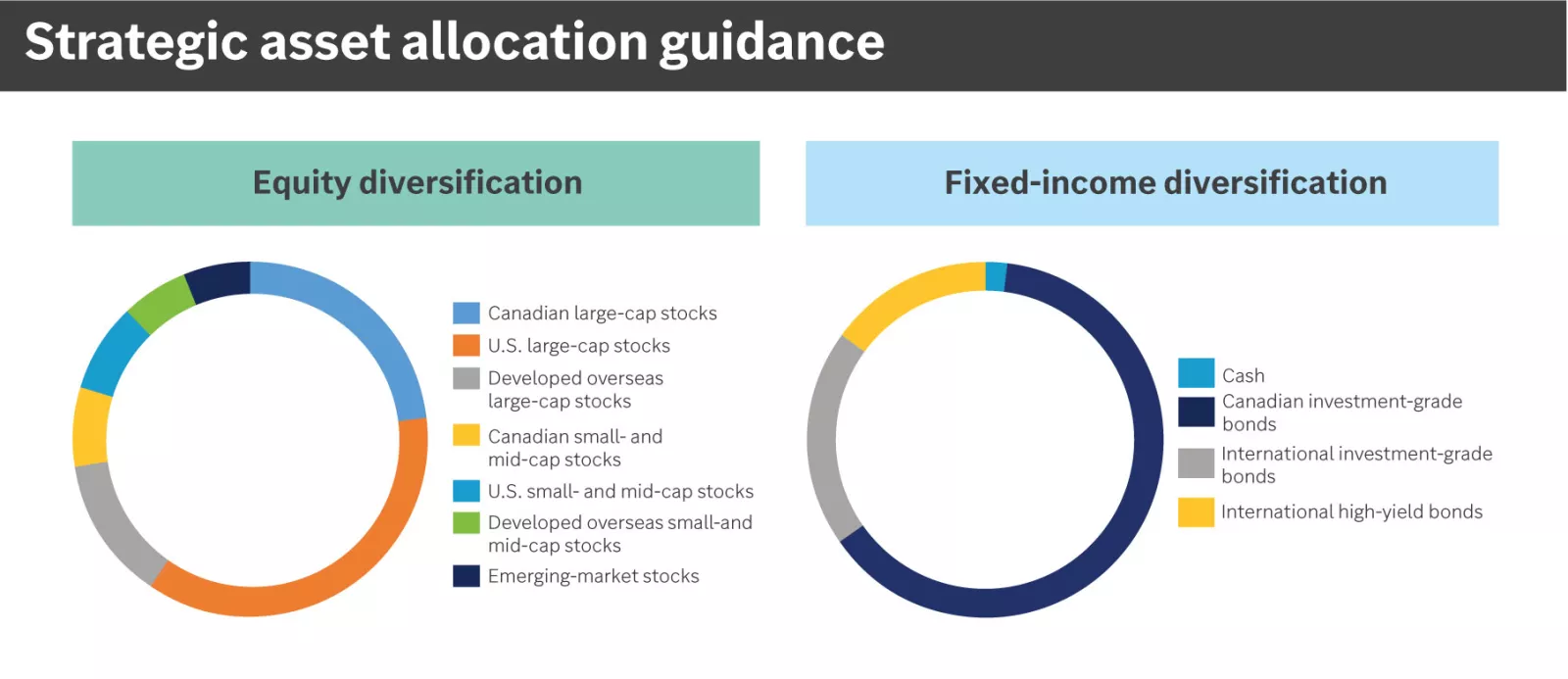

Strategic portfolio guidance

Defining your strategic investment allocations helps to keep your portfolio aligned with your risk and return objectives, and we recommend taking a diversified approach. Our long-term strategic asset allocation guidance represents our view of balanced diversification for the fixed-income and equity portions of a well-diversified portfolio, based on our outlook for the economy and markets over the next 30 years. The exact weightings (neutral weights) to each asset class will depend on the broad allocation to equity and fixed-income investments that most closely aligns with your comfort with risk and financial goals.

Diversification does not ensure a profit or protect against loss in a declining market.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: Canadian large-cap stocks, U.S. large-cap stocks, developed overseas large-cap stocks, Canadian small- and mid-cap stocks, U.S. small- and mid-cap stocks, developed overseas small- and mid-cap stocks, emerging-market stocks.

Fixed-income diversification: Canadian investment-grade bonds, international bonds, international high-yield bonds, cash.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: Canadian large-cap stocks, U.S. large-cap stocks, developed overseas large-cap stocks, Canadian small- and mid-cap stocks, U.S. small- and mid-cap stocks, developed overseas small- and mid-cap stocks, emerging-market stocks.

Fixed-income diversification: Canadian investment-grade bonds, international bonds, international high-yield bonds, cash.

Opportunistic portfolio guidance

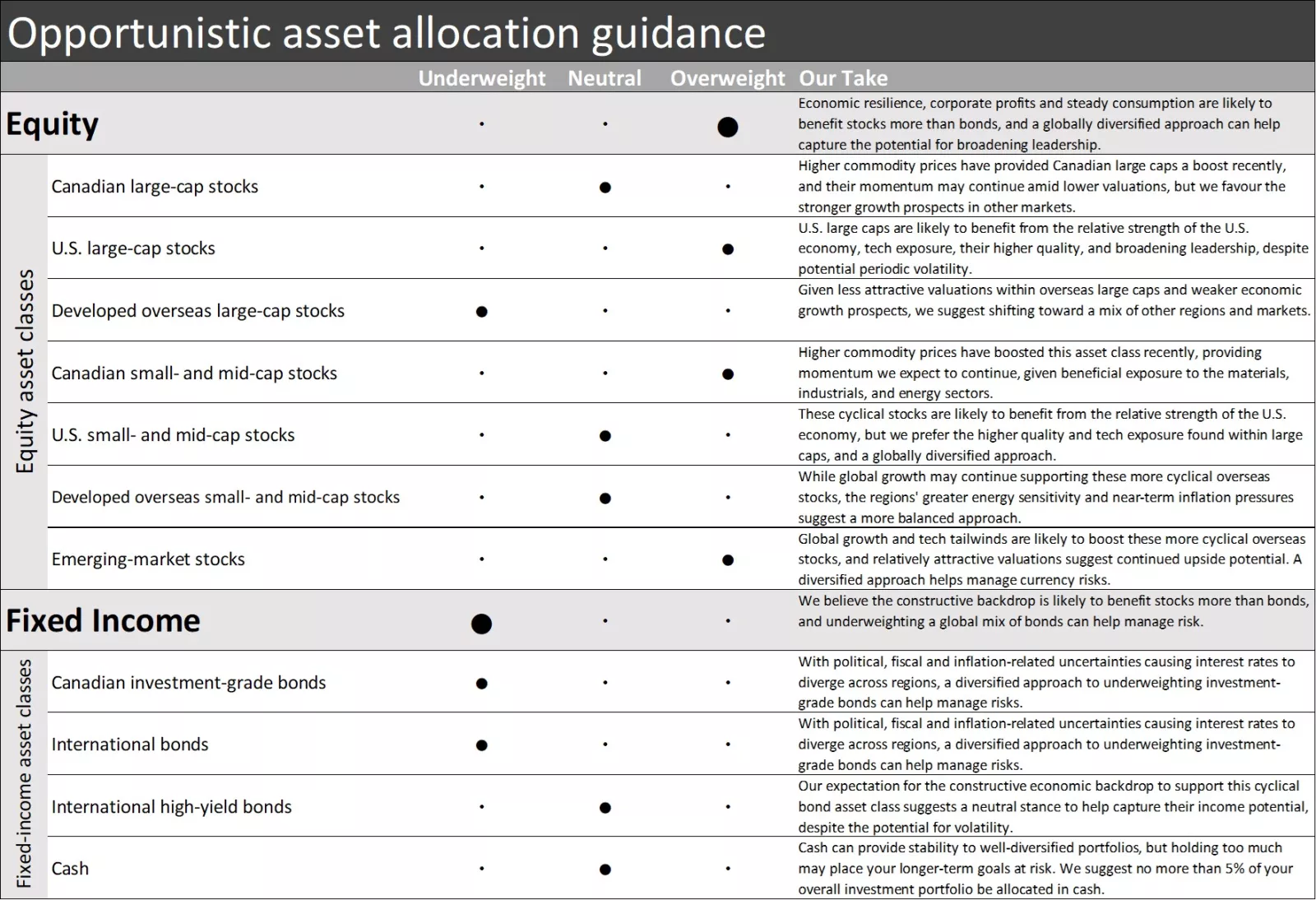

Our opportunistic portfolio guidance represents our timely investment advice based on current market conditions and a shorter-term outlook. We believe incorporating this guidance into a well-diversified portfolio may enhance your potential for greater returns without taking on unintentional risks, helping to keep your portfolio aligned with your risk and return objectives. We recommend first considering our opportunistic asset allocation guidance to capture opportunities across asset classes. We then recommend considering opportunistic equity sector and Canadian investment-grade bond guidance for more supplemental portfolio positioning, if appropriate.

Our opportunistic asset allocation guidance is as follows:

Equity —overweight overall; underweight — Developed overseas large-cap stocks; neutral — Canadian large-cap stocks, U.S. small- and mid-cap stocks and developed overseas small- and mid-cap stocks; Overweight — U.S. large-cap stocks, Canadian small- and mid-cap stocks and emerging-market stocks.

Fixed income —underweight overall; underweight – Canadian investment-grade bonds and international bonds; neutral — international high-yield bonds and cash.

Our opportunistic asset allocation guidance is as follows:

Equity —overweight overall; underweight — Developed overseas large-cap stocks; neutral — Canadian large-cap stocks, U.S. small- and mid-cap stocks and developed overseas small- and mid-cap stocks; Overweight — U.S. large-cap stocks, Canadian small- and mid-cap stocks and emerging-market stocks.

Fixed income —underweight overall; underweight – Canadian investment-grade bonds and international bonds; neutral — international high-yield bonds and cash.

Our opportunistic Canadian equity sector guidance follows:

Overweight for energy, industrials, and materials

Neutral for technology, health care, real estate, and utilities

Underweight for communication services, consumer discretionary, consumer staples, and financial services and financial services

Our opportunistic Canadian equity sector guidance follows:

Overweight for energy, industrials, and materials

Neutral for technology, health care, real estate, and utilities

Underweight for communication services, consumer discretionary, consumer staples, and financial services and financial services

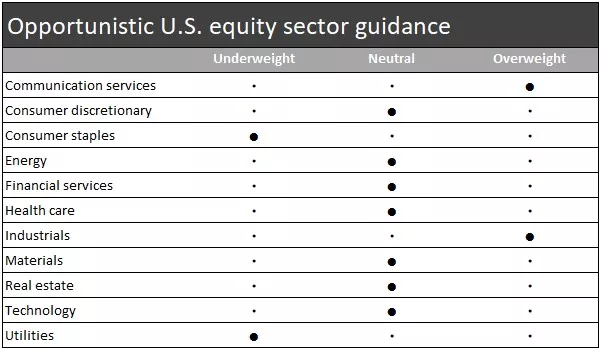

Our opportunistic U.S. equity sector guidance follows:

• Overweight for communications services and industrials

• Neutral for consumer discretionary, financial services, energy, real estate, technology, health care and materials

• Underweight for consumer staples and utilities

Our opportunistic U.S. equity sector guidance follows:

• Overweight for communications services and industrials

• Neutral for consumer discretionary, financial services, energy, real estate, technology, health care and materials

• Underweight for consumer staples and utilities

Our opportunistic Canadian investment-grade bond guidance is overweight in interest rate risk (duration) and neutral in credit risk.

Our opportunistic Canadian investment-grade bond guidance is overweight in interest rate risk (duration) and neutral in credit risk.

Tom Larm, CFA®, CFP®

Tom Larm is a Portfolio Strategist on the Investment Strategy team. He is responsible for developing advice and guidance related to portfolio construction, asset allocation and investment performance to help clients achieve their long-term financial goals.

Tom graduated magna cum laude from Missouri State University with a bachelor’s degree in finance. He earned his MBA from St. Louis University, is a CFA charter holder and holds the CFP professional designation. He is a member of the CFA Society of St. Louis.

Important information

Past performance of the markets is not a guarantee of future results.

Diversification does not ensure a profit or protect against loss in a declining market.

Investing in equities involves risk. The value of your shares will fluctuate, and you may lose principal. Mid- and small-cap stocks tend to be more volatile than large-company stocks. Special risks are involved in international and emerging-market investing, including those related to currency fluctuations and foreign political and economic events.

Rebalancing does not guarantee a profit or protect against loss and may result in a taxable event.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

The opinions stated are as of the date of this report and for general information purposes only. This information is not directed to any specific investor or potential investor, and should not be interpreted as a specific recommendation or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.