Are you investing too conservatively (or not at all) in hopes of avoiding market declines? If so, we think that’s a mistake. The biggest risk you face is not in the stock market — it’s the possibility of not reaching your long-term goals.

When it comes to investing, there are several components to risk. Understanding them can help give you the confidence to take the appropriate and necessary risks to help reach your goals.

Your risk level covers three main areas

What is risk tolerance? Risk tolerance describes your emotional comfort with risk. Knowing your comfort level with risk can help you avoid some emotional investing mistakes, such as chasing performance.

Gauging your comfort with risk is important because it’s unlikely you can reach your long-term goals if you abandon your strategy during inevitable short-term market declines. Typically, your financial advisor will ask you to complete a questionnaire that can help gauge how you might react to risk in different situations.

What is risk capacity? This describes how much risk you can afford to take. Your investment time horizon is often one of the biggest determining factors here. When you’re younger, you have more time to recover from potential declines and could reasonably handle more volatility. If you’re retired, however, you generally can’t afford to take as much risk, especially if you’re taking withdrawals from your portfolio.

What is required risk? This describes how much risk you may need to take to help reach your goals. In general, the higher the return needed, the more potential risk you’ll have to take.

Sometimes there's a gap between how much risk you’re comfortable taking, how much you can afford to take and how much you may need to take to help achieve your goals. This is where you may have to make some important decisions — and where your financial advisor can help.

All about balance

Investing is all about balance, including balancing the return you need to reach your goals in relation to your comfort level with risk. Your Edward Jones financial advisor can help ensure you’re not taking too much risk and have quality, long-term investments designed to help you reach your goals.

If you have some time before you plan to retire, it’s important to focus on the long term and consider growth investments, such as stocks and stock mutual funds, as part of your investing strategy.

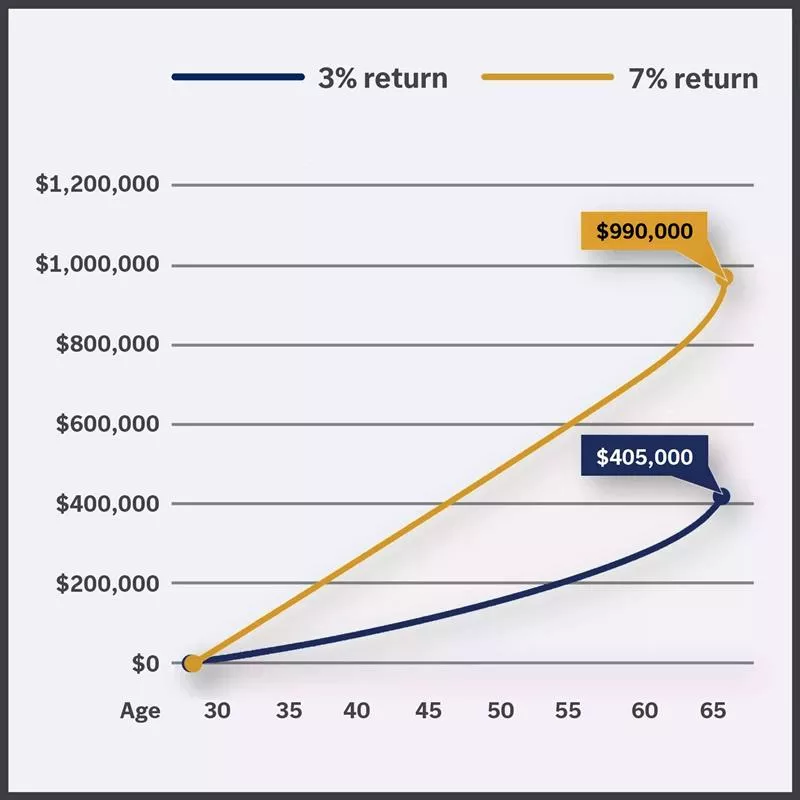

To put the importance of growth into more perspective, take a look at the chart below. The difference between a 7% return and a 3% return isn’t simply 4%: It could be nearly $600,000 for your retirement, depending on your contributions and how long you have until you retire.

Same contributions: Different returns, different results

This graph shows two lines representing the same contribution to investing over time: saving $550 per month starting at age 30. One line represents those contributions earning a 7% return for a total of $990,000 at age 65. The other line represents the same contributions earning only a 3% return for a total of $405,000 at age 65, for a difference of nearly $600,000 at retirement.

This graph shows two lines representing the same contribution to investing over time: saving $550 per month starting at age 30. One line represents those contributions earning a 7% return for a total of $990,000 at age 65. The other line represents the same contributions earning only a 3% return for a total of $405,000 at age 65, for a difference of nearly $600,000 at retirement.

If you don’t invest appropriately, the potential size of your portfolio — and your lifestyle in retirement — could be affected. So, what does this mean for your investment strategy? It depends on how long you have until you plan to retire.

If retirement is still far away

In general, if you’re many years away from retiring, more of your investments should be geared toward those that provide growth opportunities, such as stocks and stock mutual funds. You generally have more time to weather short-term declines and pursue higher long-term returns. It’s still important to own bonds, however, because they can help smooth out changes in your portfolio’s value over time.

If you’re closer to retiring

As you near retirement, it’s harder to weather larger potential market declines. Your portfolio should start becoming more balanced between stocks and bonds in the years before you retire. Your Edward Jones financial advisor can help you position your investments to provide for the first few years of your retirement income needs, balanced with the growth needed to provide income for your later years.

The key is finding balance: not taking on too much investment risk, while ensuring you have enough growth potential to help reach your long-term goals.

How we can help

Talk to your Edward Jones financial advisor today to make sure your strategy is best positioned to help you reach your goals.

Important information:

Content is provided for educational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.