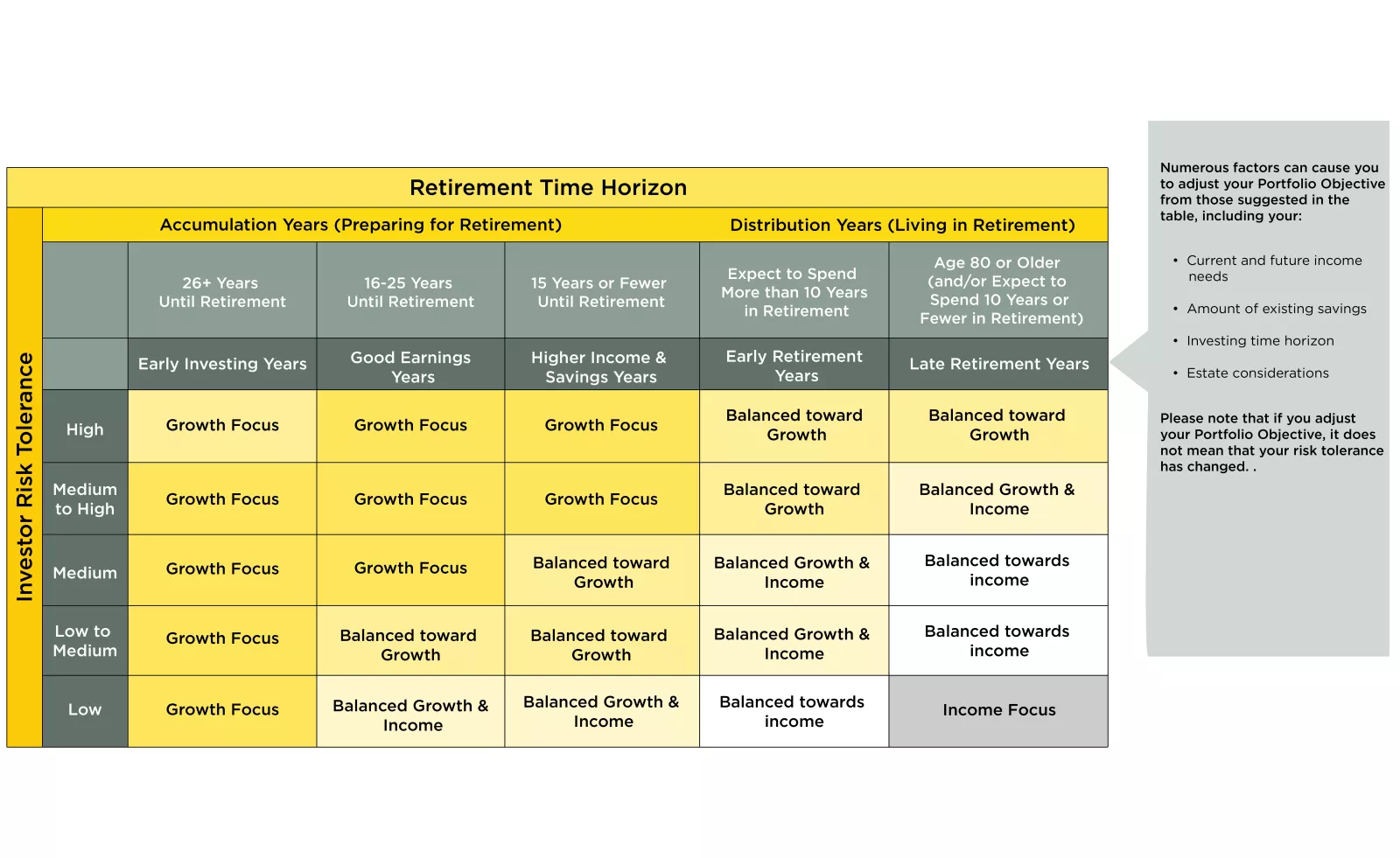

Numerous factors can cause you to adjust your Portfolio Objective from those suggested in the table, including your: Current and future income needs; Amount of existing savings; Investing time horizon; and Estate considerations. In general, your risk tolerance decreases as you age and head toward retirement. In your early investment years much of your focus may be on growth and you may wish to chose higher risk investments. As you age into your good-to-best earning years, having a balanced portfolio in terms of risk and growth is common. In early retirement and into later retirement, your portfolio may benefit by lower-risk choices and an increased interest in building and maintaining income with your investments. Please note that if you adjust your Portfolio Objective, it does not mean that your risk tolerance has changed.

There is no "one-size-fits-all" investment strategy. That's because you invest to achieve what's most important to you—whether that's retirement security, funding education, leaving a legacy, or other meaningful financial goals.

That's why your local Edward Jones financial advisor will take the time to understand your complete financial picture and work with you to develop a personalized financial plan. Your investment portfolio is a critical component of that plan, designed to help you work toward what matters most.

Investment management within your financial plan

A comprehensive financial plan addresses multiple aspects of your financial life: retirement planning, income strategies, education funding, estate considerations, and risk management. Your investment portfolio is the engine that helps power these goals.

Before we recommend investments, we ask the right questions to better understand your goals, life stage, and risk tolerance. This ensures your portfolio aligns with your broader financial objectives.

Building your investment portfolio

The steps below can help you identify a portfolio objective that you and an Edward Jones financial advisor can use as a starting point to help build a portfolio that's the right fit for you.

1. Consider your life stage

It's important to understand how your life stage impacts your financial situation. For example, if you're younger and retirement is a long way off, your investments will probably look different than if you're planning to retire in five years.

We've identified five investing stages of life: three “accumulation” phases for investors saving for retirement and two “distribution” phases for those in retirement.

The accumulation stages

Because most investors will spend more than 20 years in retirement, these stages are a critical first step in working toward building wealth and generally defined as the following:

- Early investing years - When you begin your first full-time job.

- Good earnings years - When you have 10 to 20 years until you retire.

- Higher income and savings years - When you have up to 10 years until retirement.

The distribution stages

Because your retirement can last about as long as your accumulation years, consider how wealth is distributed during the following two stages in retirement:

- Early retirement years - When you still have 15 years or more to rely on your investments for retirement income.

- Late retirement years - When you have fewer than 15 years to rely on your investments for retirement income.

2. Weigh your risk tolerance

Your risk tolerance, or how much risk you're comfortable taking, makes a big difference when choosing appropriate investments. Different types of investments carry different levels of risk—but also offer different levels of return potential. Find the right balance between the risk you’re willing to accept and the returns you anticipate receiving. Then, you’ll be in a better position to stick with your investment strategy regardless of what the market is doing. An Edward Jones financial advisor will walk you through a series of questions so you both can gain a better understanding of your risk tolerance before implementing any strategies.

3. Identify a portfolio objective

A portfolio objective helps you and an Edward Jones advisor determine the mix of investments that's right for you. Any one of five portfolio objectives could be appropriate for your long-term goals and unique financial situation. Use the Portfolio Objective Guidance Table below as a guide. First, find your life stage across the top. Then, estimate your risk tolerance using the descriptions on the right side.

The portfolio objectives that closely map to both your life stage and your risk tolerance may make sense for your situation, especially if your primary goal is retirement income. But remember, this is just a starting point for your meeting with your financial advisor. Together, you'll discuss your goals, comfort level with risk and your entire financial situation to help build a portfolio that makes sense for your situation.

Portfolio Objective Guidance Table

Source: The Portfolio Objective Guidance Table as determined by the Edward Jones Investment Policy Committee

The purpose of this table is to help you determine your portfolio objective, whether it's focused on growth, or income or something in between. It's a matrix based on two key factors. The first factor is where you're at in your investor life stage – early investing years, good earnings years, higher income and savings years, early retirement years and late retirement years. The second factor is an estimate of your risk tolerance – high, medium to high, medium, low to medium and low. Where these two factors come together in the matrix is your recommended portfolio objective. For example, if you're in your early investing years and have a high risk tolerance, a growth focus may be appropriate. If you're in your late retirement years and have a low risk tolerance, an income focus may be more appropriate.

Work with an Edward Jones financial advisor

Your Edward Jones advisor will help you build a customized investment portfolio and help you understand how each component fits into your retirement and other financial goals.

As the market shifts over time, your investments may not always be aligned with your original investment mix. Your financial goals or current situation may change. That's why your Edward Jones advisor will work with you to regularly review your portfolio and make any necessary changes.

Talk to your local Edward Jones advisor today to begin building a strategy that's the right fit for you.