First quarter economic data is out – What does it imply for investors?

Key takeaways

- Markets closed last week hopeful that a U.S.–Iran peace deal will finally help unwind the shock to global energy markets seen this year, with equities hitting new record highs and bonds rebounding.

- While uncertainty around geopolitics remains an overhang still, investors should be laser focused on underlying fundamentals, and last week's GDP reports provide useful snapshots of where things stand.

- U.S. growth looks resilient, underpinned by solid consumer spending and booming business investment, particularly around AI related outlays which are contributing meaningfully to growth.

- The U.S. national accounts also reported robust corporate profits, mirroring the signals we see in listed equities. Against this backdrop we remain constructive on stocks, even if returns might be slower and bumpier from here.

- Canadian data were more concerning, with a marginal decline in growth over Q1 pushing the economy into a technical recession after a contraction in the fourth quarter as the economy continues to lose steam.

- Finally, inflation pressures are uncomfortably hot in both economies. We remain skeptical that the Fed or Bank of Canada will hike rates but think that cuts are off the table for now, limiting the scope for further progress in bond markets.

Clear waters?

Markets hit new record highs last week on reports of an extended ceasefire between the U.S. and Iran that would finally reopen the Strait of Hormuz. This news propelled a ninth consecutive weekly gain in the S&P 500 index and a rebound in bond markets as oil prices fell to $87 per barrel.

It is worth sounding a note of caution here. We have seen false dawns around a potential reopening of the Strait in recent weeks, and we will need to see a durable recovery in traffic to be fully confident that this shock is easing.

However, the latest signals are encouraging, and if oil risks are receding then investors should be laser focused on the underlying economic and market fundamentals for clues on what the rest of the year might look like. Last week's GDP reports provide a great snapshot of how these are shaping up.

Noisy headlines but solid U.S. growth

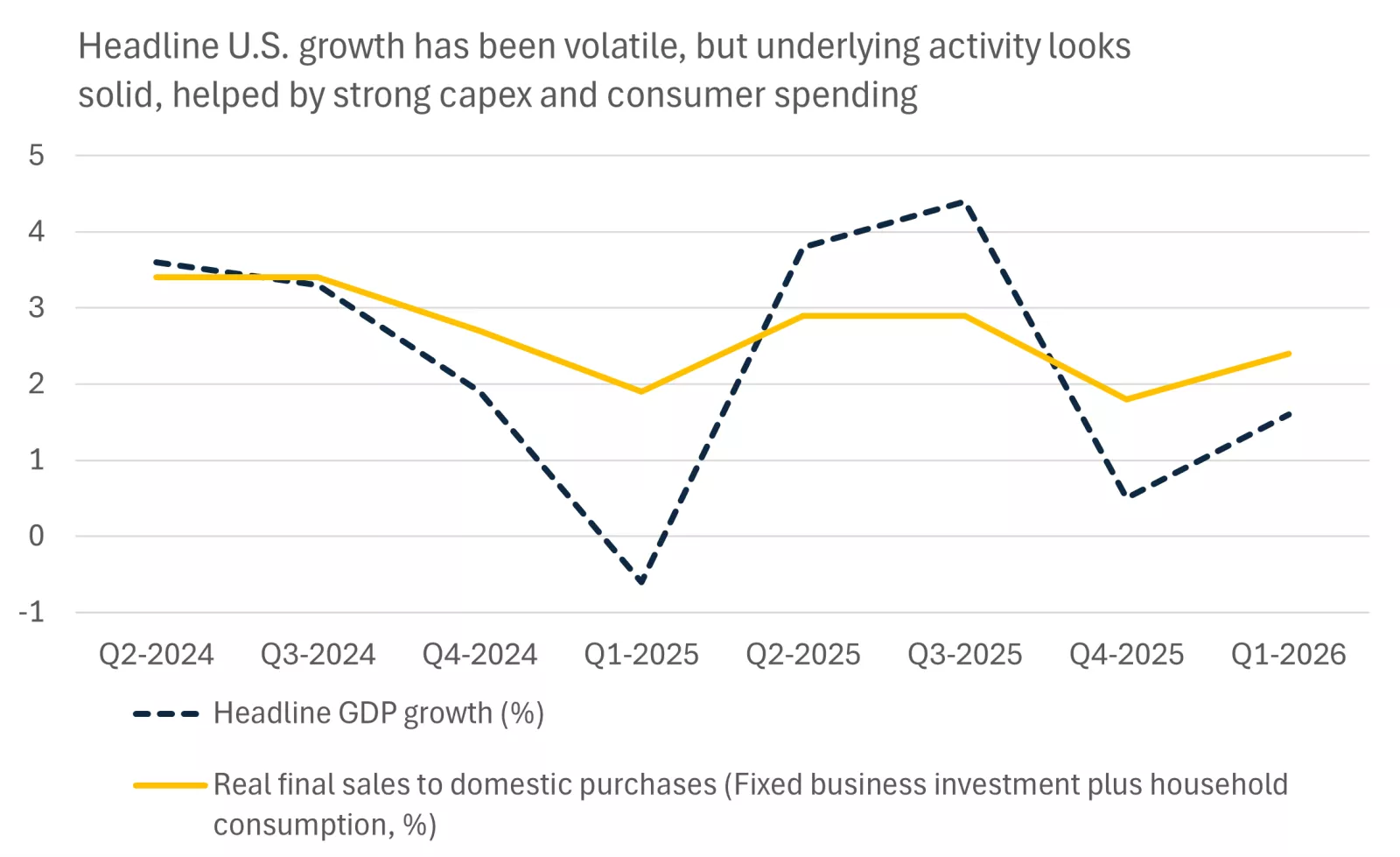

Headline U.S. GDP growth at the start of 2026 was revised lower to a soft 1.6% annualized, seemingly pointing to weak activity, especially given the soft 0.5% print in Q4 last year.

However, we always need to take care when interpreting national accounts data. Growth has been dampened by volatile components of GDP in recent quarters, including inventories and trade flows, which have been especially erratic as businesses adjust to changing tariff rates.

If we instead focus on business fixed investment and consumer household spending, this typically offers a better measure of underlying growth. According to this measure growth has been steadier, averaging a healthier looking 2.2% over the past six months.

This chart shows that headline GDP growth has been volatile from quarter-to-quarter, but the underlying trend in growth, proxied by business investment and consumer spending, looks solid.

This chart shows that headline GDP growth has been volatile from quarter-to-quarter, but the underlying trend in growth, proxied by business investment and consumer spending, looks solid.

Looking forward, while some recent data have been disappointing – particularly around the housing market – underlying growth continues to track solid gains. Durable goods orders, a timely indicator of business investment, point to strong capex. Meanwhile, consumer spending edged higher in April despite an ongoing inflation squeeze, as households dip into savings and tax refunds to smooth through this shock.

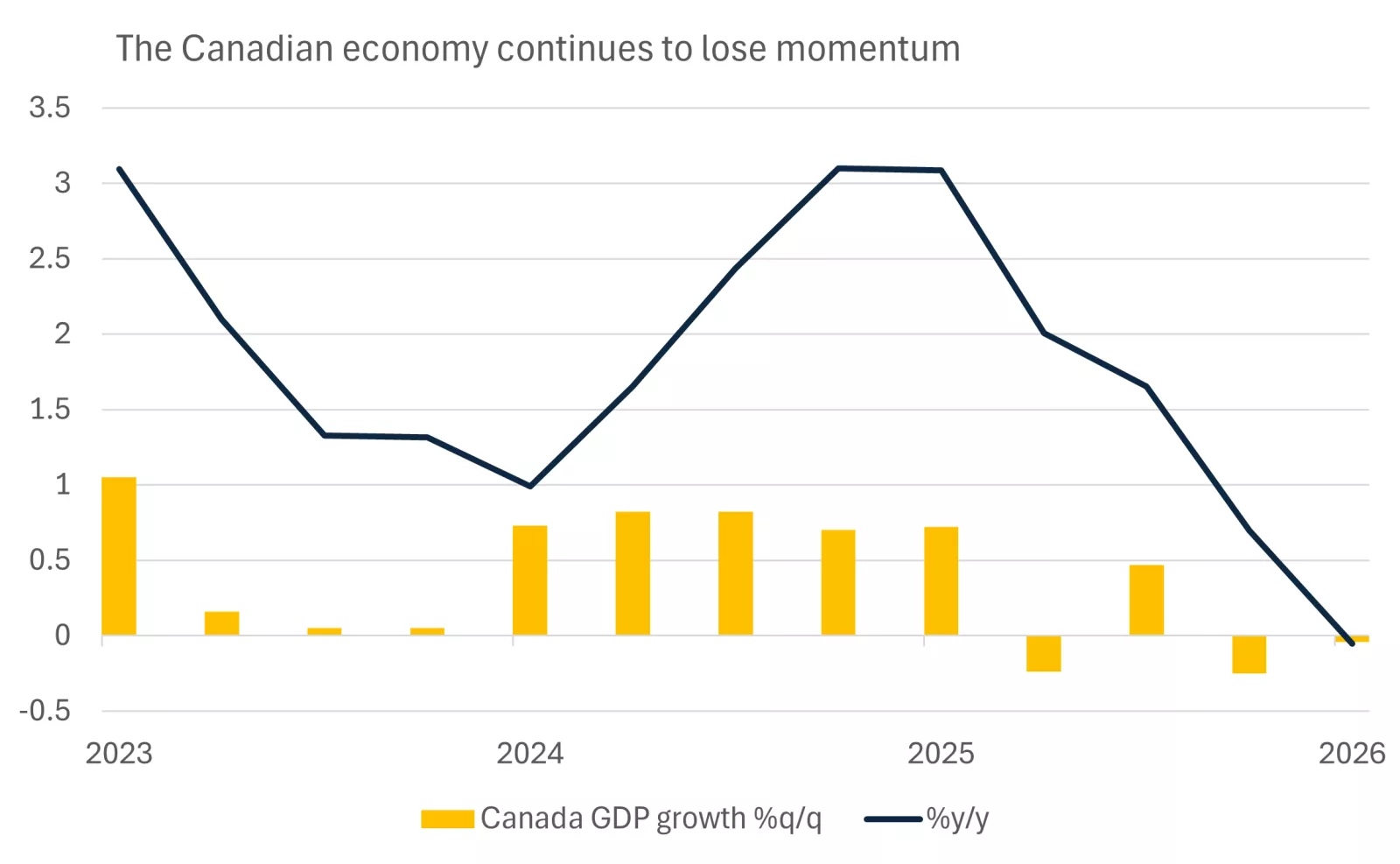

The picture in Canada is more concerning. The economy contracted slightly in Q1 according to preliminary data, pushing the economy into a technical recession following the larger decline in activity at the end of 2025.

Similar to the U.S. volatile components like net trade and inventories were a drag. However, business investment was also weak, falling 3% over the quarter annualized, and household spending at 1.5% was not sufficient to prop up growth. The Q1 disappointment chimes with the deterioration in the labour market seen so far this year and other subdued activity indicators.

This chart shows that Canadian GDP has shrunk over the past two quarters, driving a sharp slowdown in the annual growth rate to a near standstill

This chart shows that Canadian GDP has shrunk over the past two quarters, driving a sharp slowdown in the annual growth rate to a near standstill

At present we don't think the Canadian economy is heading for a full-blown recession, characterized by a deep and sustained contraction in activity. Instead, these data reflect an economy that is struggling in the face of multiple shocks, not least trade policy uncertainty, which should remain a headwind as CUSMA negotiations proceed over the summer.

Bottom line: The U.S. economy continues to remain resilient providing a solid foundation for markets, but stuttering growth in Canada underlines sluggish momentum in this economy.

AI investment an increasing driver of growth

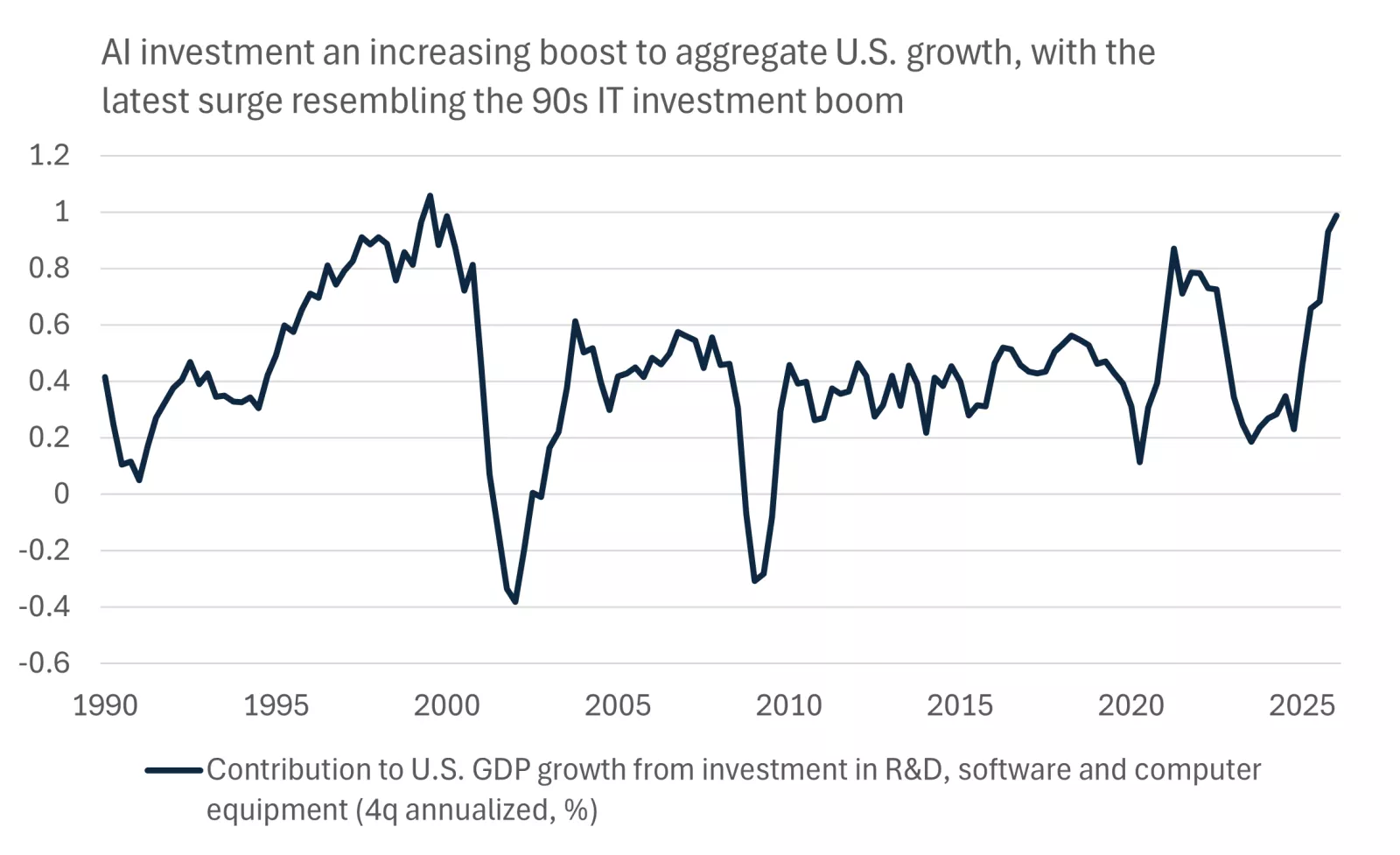

We continue to read headlines from the major AI players around eye-popping investments in AI infrastructure and technology. This spending is increasingly showing up in hard data U.S. data.

Aggregate business investment in Q1 was up an impressive 6.4% annualized, and digging deeper AI spending is driving these gains. Investment in informational processing equipment, software and R&D have all surged, contributing a full 1 percentage point to headline GDP growth over the past year.

Benchmarking this surge historically provides some useful perspective. The pickup in investment is the largest seen since the IT investment cycle of the 90s, which lasted for multiple years and delivered at its peak even larger contributions to growth. Might we see a similarly sustained cycle again?

This chart shows the rising contribution to U.S. GDP growth from investment in AI over recent quarters

This chart shows the rising contribution to U.S. GDP growth from investment in AI over recent quarters

Certainly, corporates are telling us that they will continue spending, and this week's news that Anthropic has been valued at near $1tn in a pre-initial public offering underlines the continued investor optimism around these technologies. Further ahead, there is also the potential for this investment to drive its own innovation and productivity gains, setting the stage for better future activity rates.

Bottom line: The AI investment frenzy is increasingly reflected by its rising footprint in economic growth. While the long-term payoff from this new technology remains uncertain, the huge investment cycle is helping underpin large cap technology names.

Strong corporate earning power

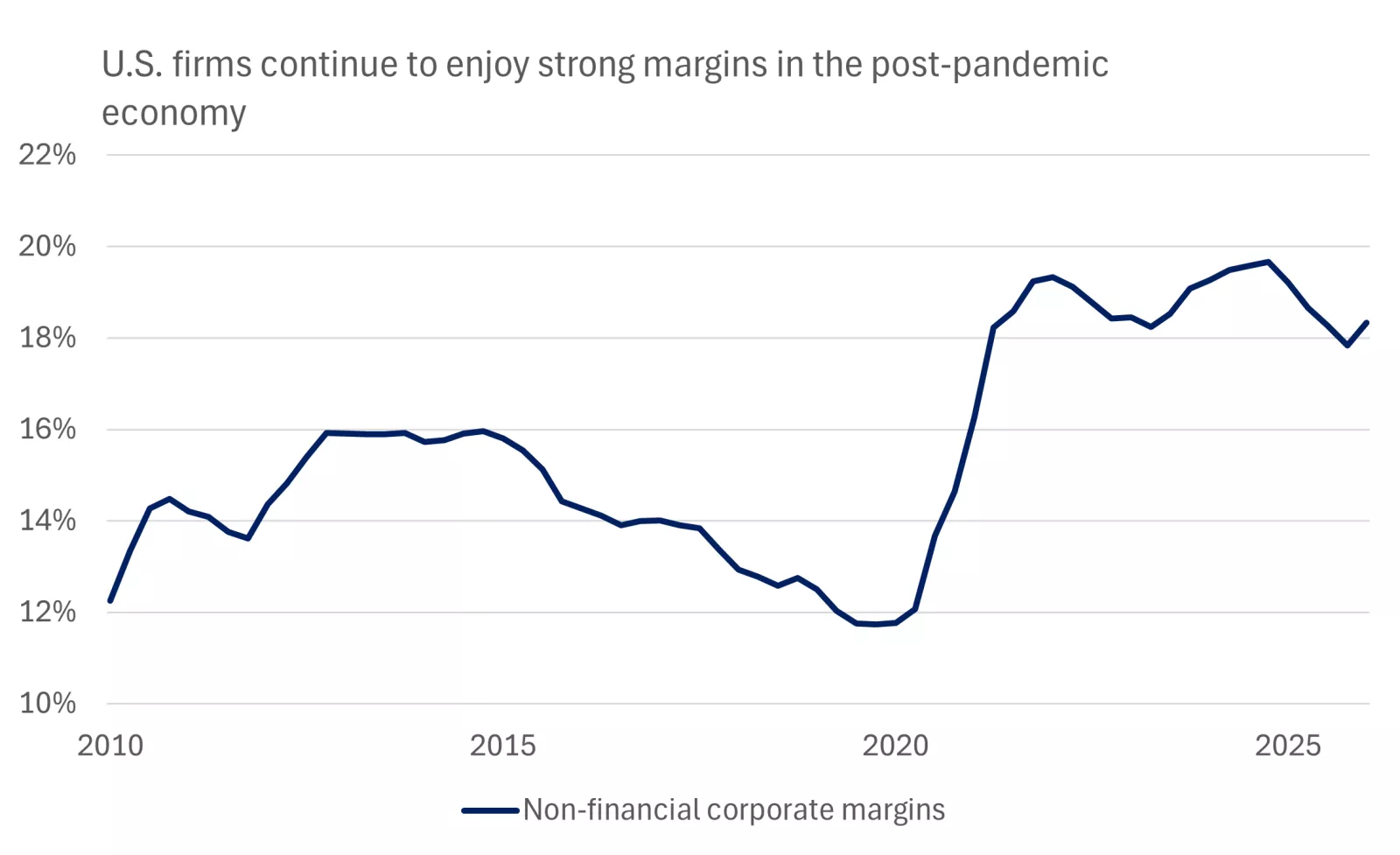

National accounts data include a wealth of information on income flows across the economy, including corporate profits. There are important differences in the calculation of GDP profits and the earnings reports we read for listed companies, and these data look at all companies, as opposed to just listed names. However, this broader measure can be a great cross-check on corporate profitability.

U.S. Q1 profits were up 3.8% annualized, at first glance not a particularly impressive gain. However, quarter-to-quarter we tend to see a good deal of volatility in profit growth, and it is better to look at the change over the past year. On this front the signal is more positive, with profits up 12%, the best reading since the post pandemic rebound in 2021 and mirroring the strong readings in Q1 corporate earnings reports.

This chart shows that non-financial U.S. firms continue to enjoy strong profit margins in the post-pandemic era

This chart shows that non-financial U.S. firms continue to enjoy strong profit margins in the post-pandemic era

Strong margins are helping underpin these earnings. Domestic non-financial corporate margins stood at 18% in early 2026 according to the latest GDP data, near post-Covid highs and comfortably above those seen before the pandemic.

Interestingly, while Canadian growth has lagged the U.S. over the past year, corporate profits as measured in the national accounts have been more closely aligned. Despite a dip in Q1 Canadian pre-tax profits are up 15% over the past year, providing a reminder that companies can still deliver earnings growth even amid weak headline economic activity rates.

Bottom line: Strong and broad earnings growth across markets this year is one of the reasons we are advocating for overweight allocations across large cap and midcap U.S. equities and other selected international markets too as we look to tap into a broadening in market leadership.

An uncomfortable inflation backdrop

The fly in the ointment of the latest U.S. GDP data were undoubtedly on the price side.

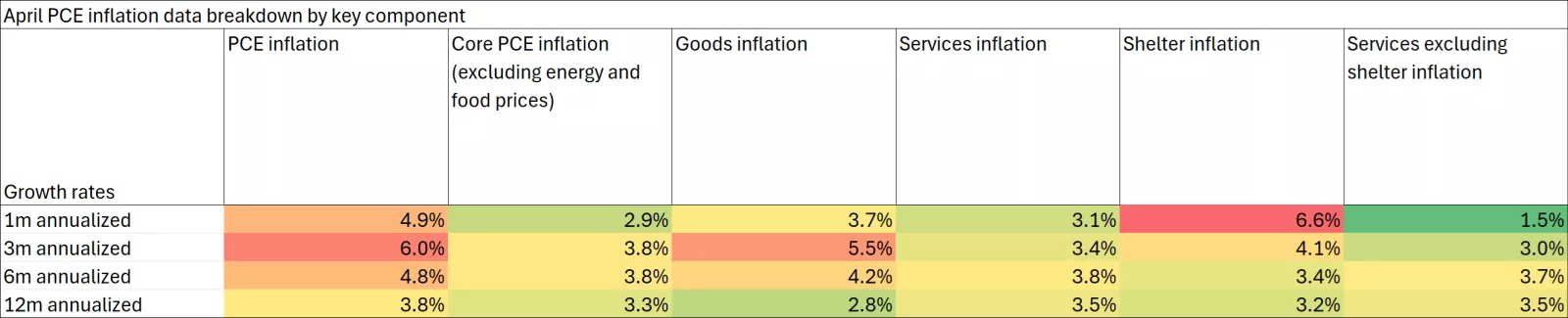

The personal spending deflator, the Fed's preferred measure of inflation, spiked to 3.5% over Q1as a whole. Worse, monthly data showed that this jumped even further in April, to 3.8%, and we expect another nudge higher in May.

This chart shows the components of U.S. PCE inflation

This chart shows the components of U.S. PCE inflation

Some of this is an oil story, as gas prices push inflation higher. However, excluding energy prices, inflation was running at 3.3% in April, well above the Fed' target for 2%. Scratching further beneath the surface, good goods prices are running unusually hot at 2.8%, while core services inflation remains elevated at 3.5%.

These data put the Fed in a tough spot, and it is interesting to see markets continue to price a hike within the next year, even as risk around oil prices seemingly ease. We think the bar for raising rates remains high, and don't expect tighter policy unless we see signs of a further pick-up in price growth, particularly on the core side. Instead, we expect the central bank to stay on hold absent any growth scare.

Canadian inflation has been somewhat better behaved over 2026 so far. Admittedly, headline CPI has spiked to 2.8%, but this acceleration has been very narrowly concentrated in energy prices. Absent these, core measures of inflation remain well behaved, and the combination of slow growth and a weak labour market should keep these pressures subdued.

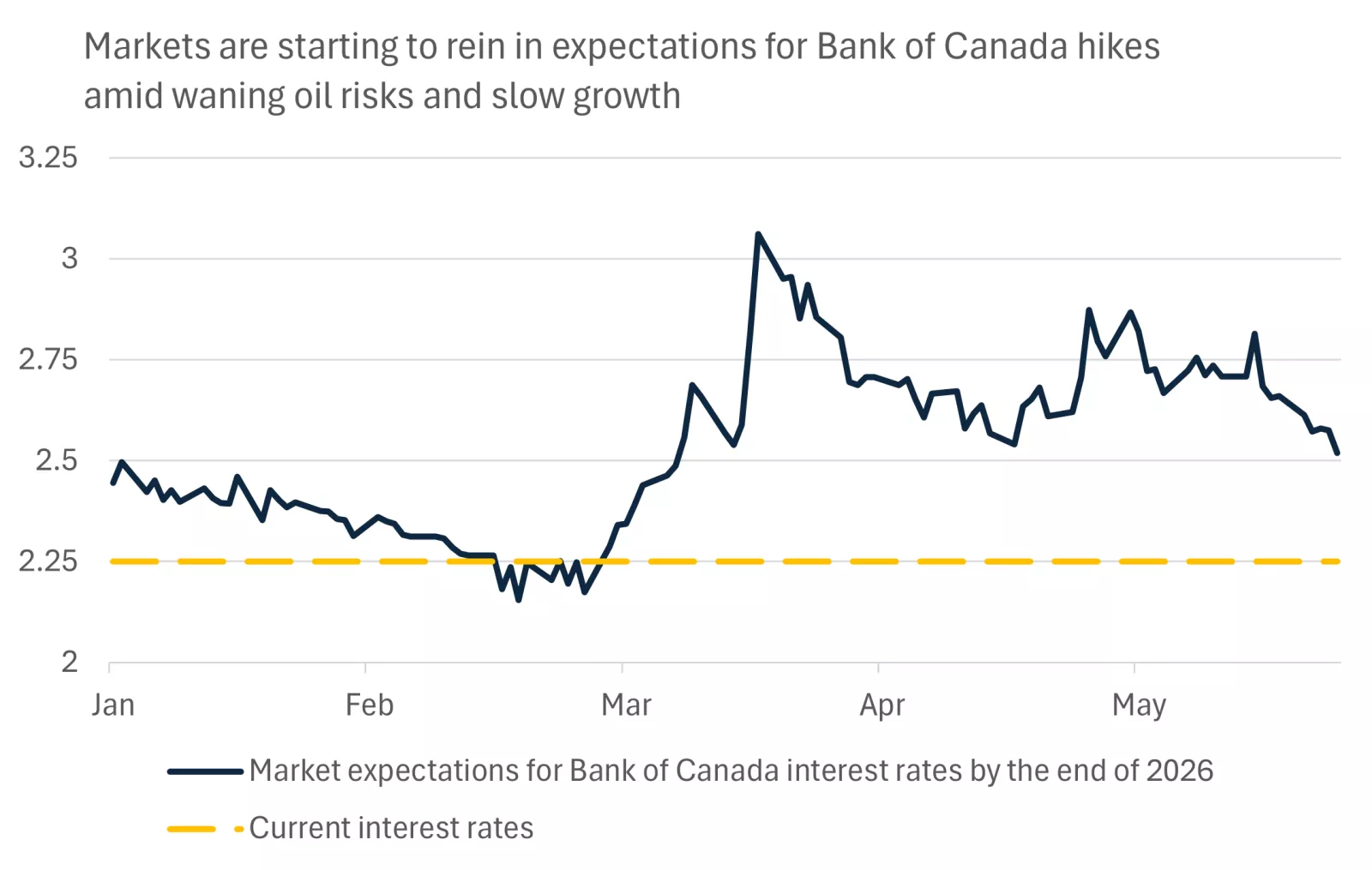

This chart shows that market expectations for rate hikes peaked in March when investors expected interest rates to rise to 3%, before softening recently to 2.5%.

This chart shows that market expectations for rate hikes peaked in March when investors expected interest rates to rise to 3%, before softening recently to 2.5%.

All in, it is not a surprise to see expectations for Bank of Canda rate hikes continue to subside. Markets had expected two or three 25 basis points hikes back in March, but now anticipate just one more. In our view this pricing still looks overdone. Weak activity rates should keep the Bank of Canada on hold this year, and arguably, the central bank would be preparing to cut absent the spike in global oil prices.

Bottom line: While bond yields have fallen from their highs further material progress will be challenging in an environment of elevated inflation.

Reading the tea leaves

Mapping the interplay of geopolitical risk, growth and inflation into markets can be challenging for investors (and even experts), especially amid uncertainty over policy and noisy data. Through all the noise this year markets have delivered excellent returns, and we remain constructive on the outlook for equities, even if there may be some twists and turns in the road ahead.

If you are feeling unsure around the outlook, working with a financial advisor can cut through some of this noise, and critically, help you stay focused on achieving your long-term financial goals.

James McCann;

Investment Strategy

Sources: All data referenced in text from Bloomberg

The Week Ahead

Important economic data and events for the week ahead include the May Labour Force Survey in Canada, and the May jobs report, manufacturing and services PMI, and productivity in the U.S.

James McCann

Senior Economist

Thought Leader In:

- Economic issues impacting the lives of everyday Americans.

- The effects of government spending, taxes and regulation changes on our clients.

- Building diversified portfolios to help investors reach their long-term financial goals.

“The economic, political and policy landscape is shifting dramatically, making it ever more challenging for our clients to navigate their personal finances. In this environment, it's our deep, research-driven insights that can help clients stay on track to reach their financial goals."

James McCann

Senior Economist

Previous weeks' weekly market wraps

Important information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved of owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent to international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.