The U.S. and Israel launched joint strikes on Iran on February 28, prompting Iran to respond with counterattacks across multiple Middle Eastern cities. Iran is a meaningful oil producer, the fourth largest within OPEC, accounting for roughly 4% of global oil supplies, with about 80% of its exports going to China. The country also occupies a strategically important position: it controls access to the Strait of Hormuz, a key chokepoint through which approximately 20% of the world’s oil supply flows.

Recent attacks on energy infrastructure have disrupted production of both oil and natural gas, while oil and liquified natural gas (LNG) tankers have been delayed or rerouted. In response, the U.S. administration announced measures to provide risk insurance to ships traveling through the region, including oil tankers.

Markets respond to short-term uncertainty

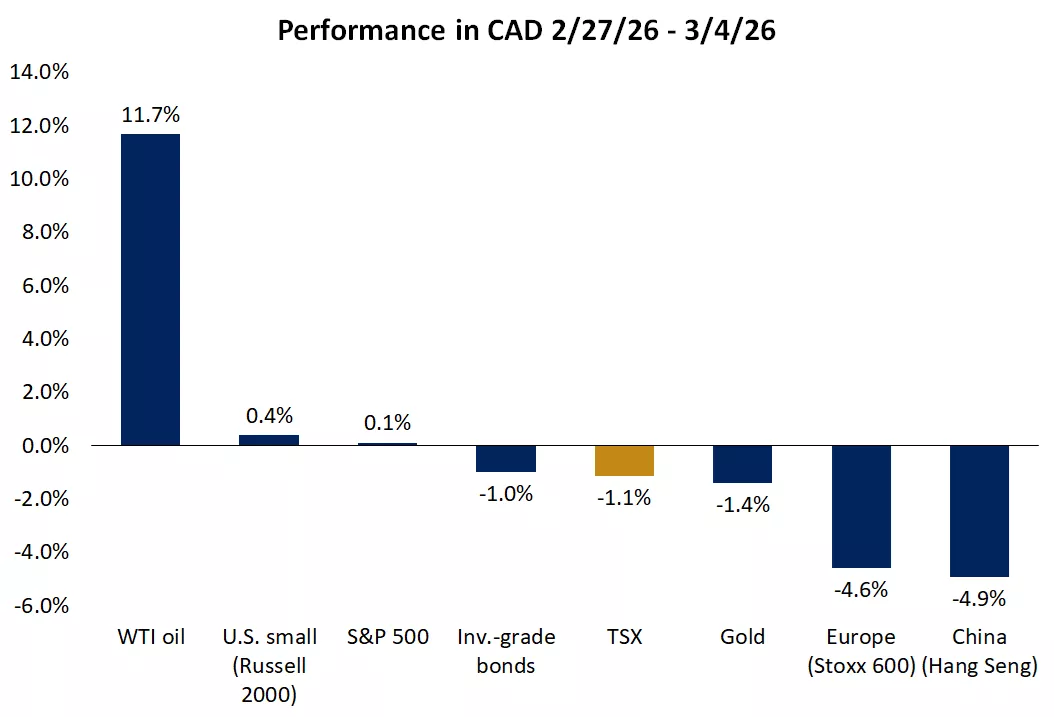

Heightened geopolitical risk and the potential for supply disruptions drove oil prices more than 10% higher since the start of military action, triggering a risk‑off response in equities. Bonds and gold held up better, though they also posted modest declines as investors weighed the possibility that higher oil prices may lift near‑term inflation and potentially delay the Fed’s anticipated rate cuts.

The U.S. dollar strengthened, reflecting its haven status, which contributed to the underperformance of overseas equities. Europe and Asia, in particular, are more dependent on imported oil that travels through Middle Eastern shipping lanes.

The graph shows performance of major assets since the start of the Iran conflict.

The graph shows performance of major assets since the start of the Iran conflict.

Three reasons why the economy and market may prove resilient

While the duration and impact of the conflict are uncertain, focusing on what we do know provides useful perspective for investors.

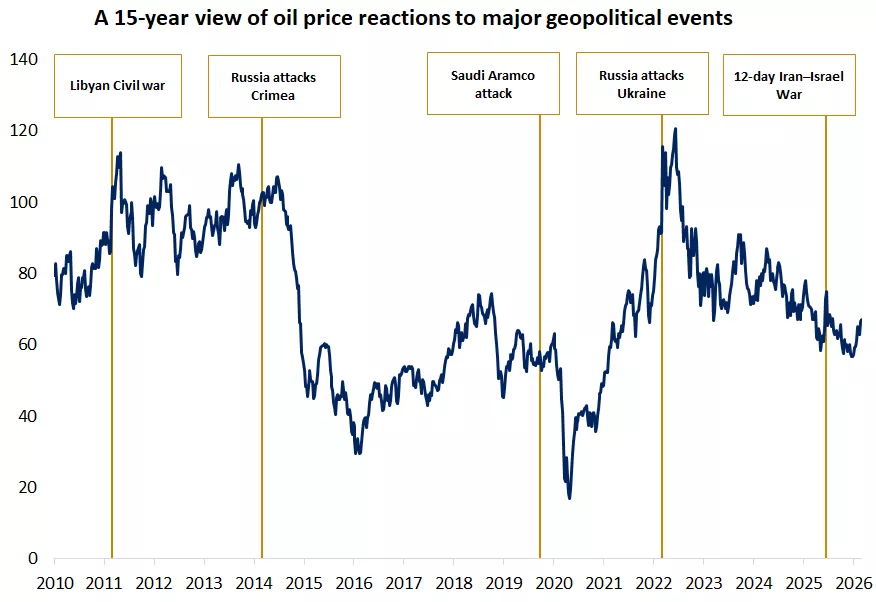

1) Historical geopolitical shocks tend to have short‑lived market impacts - Over the past 15 years, multiple geopolitical events have produced temporary oil spikes with limited broader market fallout. Oil prices often rise ahead of major events and peak shortly after. For example, WTI peaked 10 days after the Israel‑Iran war in summer 2025 and three months after Russia’s invasion of Ukraine.

The graph shows oil prices along with major geopolitical risk events over the past 15 years.

The graph shows oil prices along with major geopolitical risk events over the past 15 years.

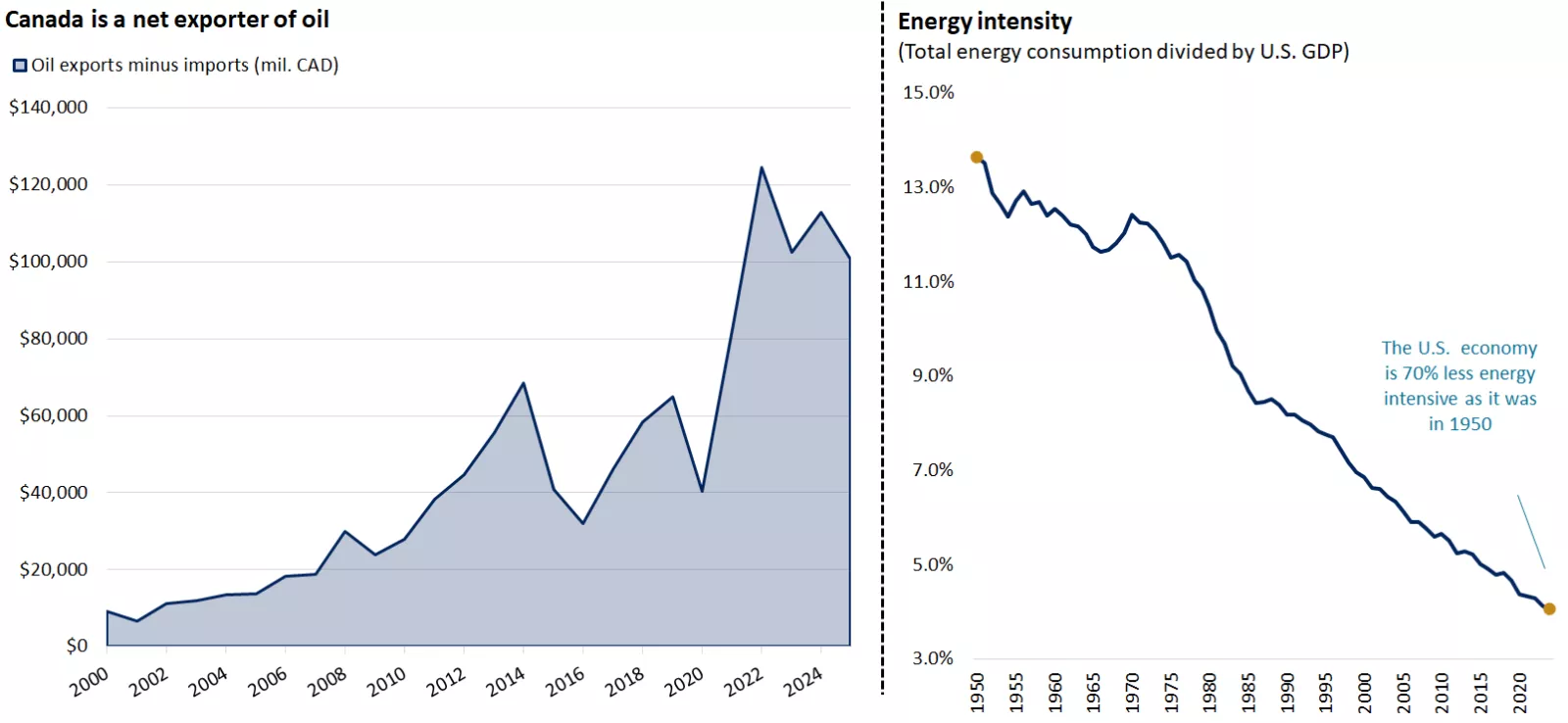

2) Canada is structurally less vulnerable to oil shocks - Canada is a significant net exporter of oil, and rising global energy prices often benefit Canadian producers, government revenues, and the broader resource sector. While consumers face higher fuel costs, the overall macroeconomic impact is more balanced than in countries reliant on imported oil. South of the border, the U.S. has been a net exporter of oil since 2019, and the economy is far less energy‑intensive than in prior decades. Since 1950, the energy required to produce one unit of U.S. GDP has fallen by roughly 70%, driven by efficiency gains and the growth of the services sector.

The graph on the left shows that Canada is a net exporter of oil. The graph on right shows how the U.S. economy is much less energy intensive than it used to be when looking at total energy consumption divided by U.S. GDP.

The graph on the left shows that Canada is a net exporter of oil. The graph on right shows how the U.S. economy is much less energy intensive than it used to be when looking at total energy consumption divided by U.S. GDP.

3) Global oil supply remains ample - The U.S. Energy Information Administration (EIA) reports that the global oil market is currently oversupplied, leading to persistent inventory builds. The Iran crisis also prompted OPEC+ to expand planned production, raising output by 206,000 barrels per day beginning in April. These dynamics may help prevent a sustained surge in oil prices.

Don't lose sight of the big picture

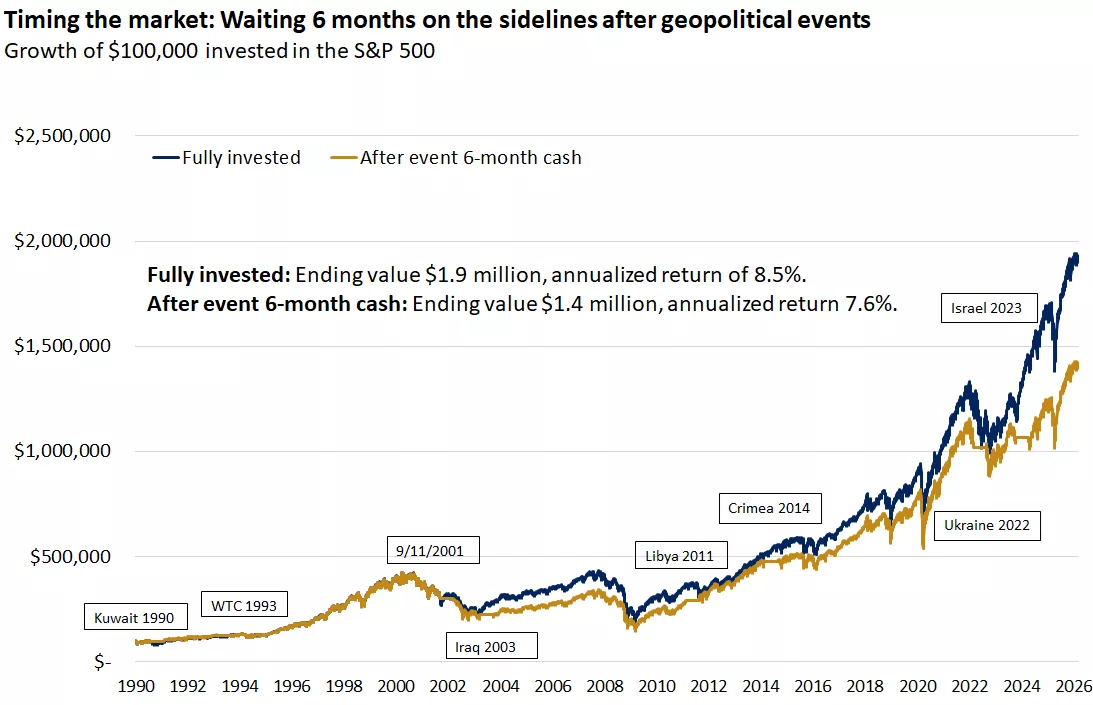

History shows that making reactionary moves, especially around global events that generate headlines but often fade quickly, has come at a real cost to long‑term returns. Remaining fully invested has historically outperformed stepping to the sidelines for three or six months while waiting for uncertainty to clear before re-entering the market*. Avoiding playing geopolitics with your portfolio may be the best course of action.

The graph shows the performance of a strategy staying invested in the S&P 500 since 1990 and another moving to cash for six months following major geopolitical events before reentering the market. Remaining fully invested has historically outperformed.

The graph shows the performance of a strategy staying invested in the S&P 500 since 1990 and another moving to cash for six months following major geopolitical events before reentering the market. Remaining fully invested has historically outperformed.

While market pullbacks are uncomfortable, the underlying macroeconomic backdrop remains supportive, in our view:

- The North American economy is on track for healthy growth.

- Corporate earnings remain strong, with TSX profits expected to grow 16% in 2026.

- The labour market appears to be stabilizing.

- The BoC's policy is at the low end of neutral, and the Fed is still likely to cut interest rates later this year.

The bottom line

The Middle East conflict remains fluid, but both historical patterns and today’s market fundamentals offer reassurance. Geopolitical flare‑ups often spark short‑term volatility but have tended to produce limited and temporary market impacts—and that remains our base‑case expectation.

This year’s broadening of market leadership helps reinforce the value of diversification. For investors underexposed to U.S. mid‑caps or overseas equities, recent volatility may create an attractive opportunity to deploy fresh capital or rebalance portfolios.

Geopolitical headlines can fuel short‑term uncertainty, but your financial strategy should remain anchored in the long term, in our view.

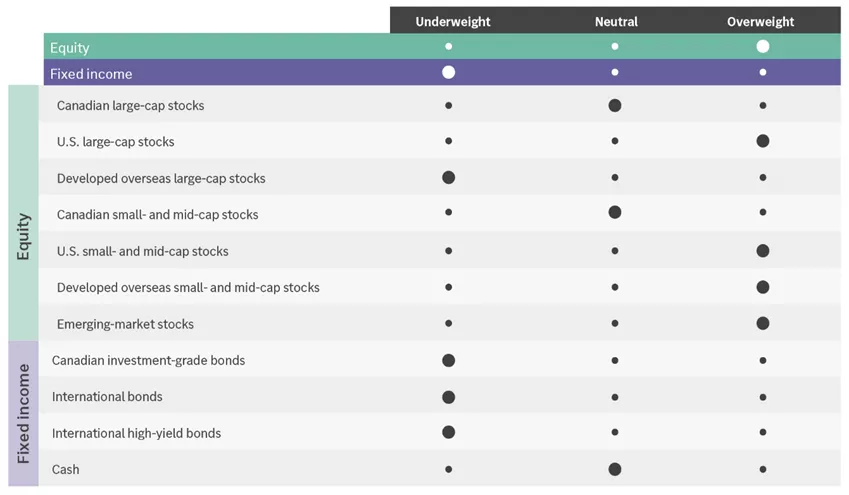

Equity —overweight overall; underweight — Developed overseas large-cap stocks; neutral — Canadian large-cap stock and Canadian small- and mid-cap stocks; Overweight — U.S. large-cap stocks, U.S. small- and mid-cap stocks, developed overseas small- and mid-cap stocks, and emerging-market stocks.

Equity —overweight overall; underweight — Developed overseas large-cap stocks; neutral — Canadian large-cap stock and Canadian small- and mid-cap stocks; Overweight — U.S. large-cap stocks, U.S. small- and mid-cap stocks, developed overseas small- and mid-cap stocks, and emerging-market stocks.

Angelo Kourkafas, CFA

Investment Strategist

Source for all data: Bloomberg, *Bloomberg, Edward Jones

Angelo Kourkafas

Angelo Kourkafas is responsible for analyzing market conditions, assessing economic trends and developing portfolio strategies and recommendations that help investors work toward their long-term financial goals.

He is a contributor to Edward Jones Market Insights and has been featured in The Wall Street Journal, CNBC, FORTUNE magazine, Marketwatch, U.S. News & World Report, The Observer and the Financial Post.

Angelo graduated magna cum laude with a bachelor’s degree in business administration from Athens University of Economics and Business in Greece and received an MBA with concentrations in finance and investments from Minnesota State University.

Important Information:

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Investing in equities involves the risk of loss. The value of an investors shares can fluctuate, and investors can lose money. Small-and mid-cap stocks tend to be more volatile than large company stocks.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.