The foundation of an effective business succession plan begins with clearly defined goals. Ask yourself:

- What do I want to achieve through this transition?

- Is my priority to keep the business in the family, maximize its sale value, ensure continuity for employees, or secure retirement income?

- Have I calculated what income and/or assets I need to achieve my goals? This may include living expenses, gifting to family or charity during my lifetime, and bequests upon death.

- How do I envision my transition? For instance, am I willing to work full time or part time post-transition to support the transition's success?

- What will I do after the transition? Do I have hobbies? Are there friends and family I'd like to spend more time with? Are there passions I want to pursue, such as sitting on a board?

Clarifying your goals early will shape every decision—from selecting a successor to structuring the financial and legal components of your plan.

Open and honest conversations with family members, business partners, and key employees are essential.

Family members may have differing expectations around ownership or involvement. Business partners and employees may need clarity to remain engaged and committed. Early conversation helps align everyone with your long-term vision and reduces the risk of misunderstandings later.

Clear communication builds trust and lays the groundwork for a smoother transition – especially in family-owned business where emotional dynamics can add complexity to decision-making.

You don’t have to navigate business succession planning alone - nor should you. A well-rounded team of professionals can guide you through each stage of the process. At the centre of this team is your financial advisor, who helps coordinate planning, execution, and post-transition support.

Other key professionals include:

- Tax Professional (CPA): Manage tax implications and optimize strategies.

- Legal Professional: Draft and review agreements, wills, and corporate documents.

- Business Valuation Expert: Determine the fair market value of your business.

- Insurance Advisor: Provide coverage for risk management and funding buy-sell agreements.

- Investment Banker or M&A Advisor: Assist with structuring and negotiating a sale, if applicable.

Having the right team in place early can save time, reduce stress, and help you avoid costly mistakes. Their expertise helps ensure your succession plan is both practical and aligned with your financial and personal goals.

Knowing the value of your business is essential—whether you're selling, transferring ownership to family, or planning for tax implications. A professional valuation helps ensure fairness and helps you make informed decisions.

A business valuation can help you:

- Set a fair price if you are selling

- Treat family members fairly if you are passing the business on

- Plan effectively for taxes and estate considerations

Professionals who can help you with business valuation include:

- Chartered Business Valuators (CBVs)

- Chartered Professional Accountants (CPAs)

- Business Advisors and Consultants

Common valuation approaches include:

Income based approach

Focuses on projected profits—ideal for businesses with stable earnings.

Asset based approach

Calculates value by subtracting liabilities from assets—often used for holding companies or inactive businesses.

Market based approach

Compares your business to similar ones recently sold, typically using a multiple of EBITDA (earnings before interest, taxes, depreciation, and amortization).

Getting a valuation early in your planning process can also reveal opportunities to enhance your business’s value—especially if you have time to make strategic improvements before the transition.

Choosing your successor is one of the most pivotal decisions in your succession plan. Ownership, management, and leadership responsibilities don’t necessarily have to be passed to the same individual—but each role must be thoughtfully considered.

Successors typically fall into two categories:

- Internal: Family members, business partners, or key employees

- External: Outside buyers or investors

In some cases, liquidation may be the preferred option if a suitable successor isn’t available or if selling the business isn’t viable.

Comparing internal vs external business successor options for business succession

Here’s a summary of the different successor paths and their potential outcomes:

| Successor path | Definition | Potential outcomes |

|---|---|---|

| Internal transfer | A sale/transfer to someone affiliated with the company, such as a family member, business partner or employees |

|

| External transfer | A sale/transfer to an unrelated third party |

|

| Liquidation | An unwinding of the business by selling individual assets to the highest bidder |

|

Whether you're passing the torch to a family member or selling to an outside buyer, the decision should reflect your values, long-term vision, and financial goals.

Once a successor is chosen, the real work begins—preparing them to lead. This involves:

- Training in key operational and strategic areas

- Mentorship to pass on your experience and values

- Leadership development through hands-on experience or external programs

- Introduction to key relationships – this may be suppliers, customers, regulators, or other relationships that help make your business successful.

Whether your successor is a family member, business partner, key employee, or external buyer, investing in your successor’s growth can be essential to help ensure a smooth and successful transition.

As you prepare for succession, it’s important to reduce risks that could disrupt your business or your family’s financial security. This means ensuring key protections and agreements are in place before you step away. Here are some areas to focus on:

1. Update shareholder agreements

Ensure agreements reflect current goals, include buy-sell provisions, and are properly funded -often with life insurance

2. Review insurance coverage

Maintain the right mix of coverage:

- Life insurance for buyouts and taxes

- Disability insurance for income protection

- Key person insurance for key employees

3. Update estate documents

Align wills, powers of attorney, and trusts with your succession plan.

4. Retain key employees

Secure top talent with retention bonuses or incentive plans.

Succession planning isn’t just about the business—it’s also about your life after the transition. Both plans should work together to help ensure financial security for you and stability for the business.

Once you've designed and reviewed your business succession plan, it is important to develop your personal Post-Transition Plan, which may include:

- Planning for retirement income and lifestyle needs.

- Reviewing your wealth and tax strategies.

- Updating estate planning documents (wills, powers of attorney, trusts).

- Considering how the transition impacts your family and long-term goals.

Your succession plan should grow and adapt alongside your life and business—it’s not a “set it and forget it” document. To keep it effective:

- Share the plan with trusted family members, business partners, and key employees.

- Communicate openly to help reduce uncertainty, foster trust, and build confidence during periods of transition.

- Review regularly every few years, or in response to major life or business events—such as marriage, divorce, the birth of a child, changes in tax legislation, or significant business growth.

These updates help ensure your plan remains relevant, aligned with your goals, and responsive to changing circumstances.

The tax and legal implications of business succession can be complex and vary depending on your chosen path. Addressing these early with the help of qualified professionals is critical in helping to protect your wealth and ensure a seamless transition. Some key considerations include:

- Lifetime Capital Gains Exemption (LCGE)

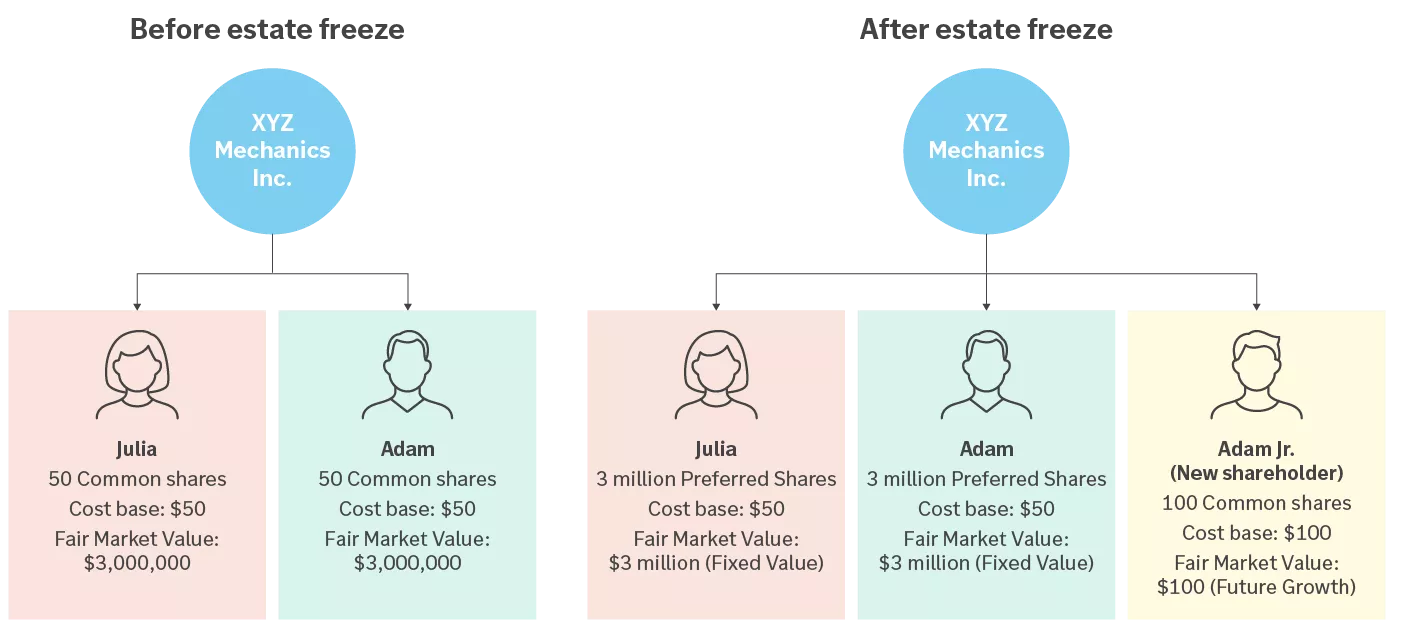

- Estate freeze

- Whether to sell assets or shares

- Shareholder agreement

In the next section we dive deeper into what you need to know about each of these elements and why they are important to consider.