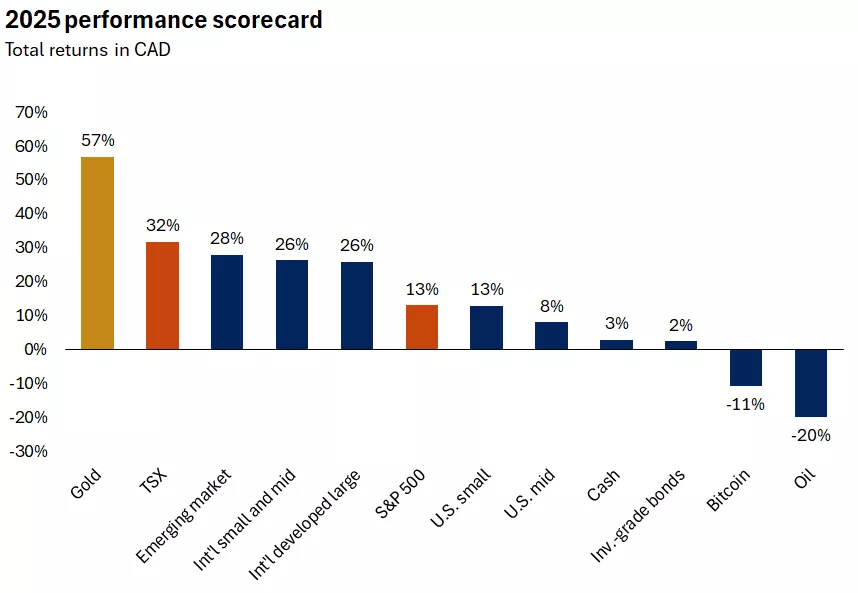

Canadian stocks delivered a stellar performance in 2025, outperforming U.S. stocks by the widest margin since 2009, driven in large part by the resource-heavy composition of the TSX *. This leadership unfolded against the backdrop of a powerful surge in commodity markets, where precious metals saw dramatic gains. Gold surged 57%, its strongest annual gain since 1979, outpacing all major asset classes, including technology stocks and other equities*. The question now is: Can this rally be repeated, and how should investors view gold as an asset class going forward?

The graph shows performance for different investments in 2025, with gold outperforming by a wide margin.

The graph shows performance for different investments in 2025, with gold outperforming by a wide margin.

What has been driving the gains?

This historic rally was fueled by a mix of factors that boosted gold’s appeal to investors. Some drivers are short-term and may prove temporary, while others are more structural. Together, they created the perfect storm for gold’s surge:

- High uncertainty and risk

- Trade uncertainty and deglobalization trends

- Rising geopolitical risks

- Fiscal and debt sustainability concerns

- Favourable macroeconomic conditions

- U.S. dollar weakness

- Declining real interest rates

- Strong demand dynamics

- Robust central bank purchases

- Price momentum and increased investment flows

Because gold is an asset that doesn’t generate cash flow or pay dividends, its appeal often depends on the opportunity cost of holding it. Real interest rates are a key driver. When they decline, gold typically benefits, and when they rise, gold tends to lag. Similarly, a weaker U.S. dollar lowers the relative cost for global investors, adding to gold’s attractiveness.

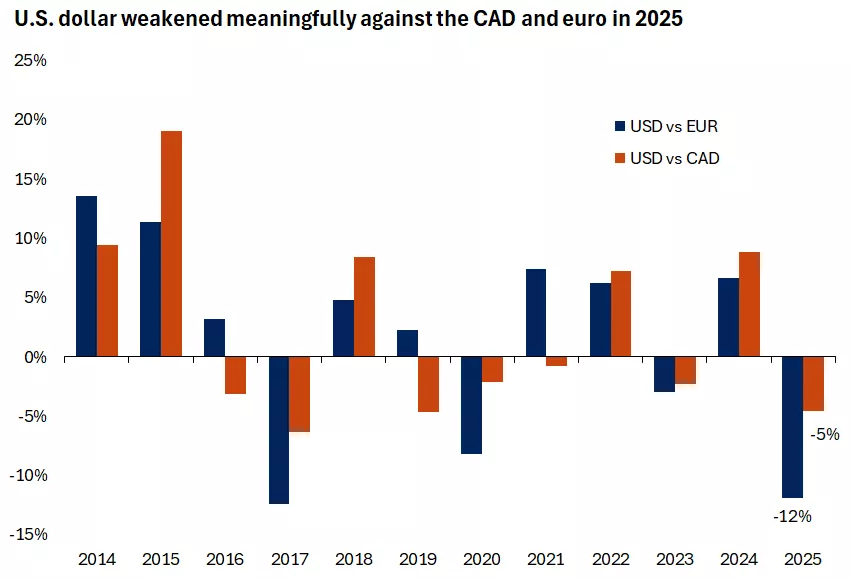

In 2025, both forces were firmly in play. Central banks shifted from restrictive to more neutral policy as inflation normalized, pushing real rates lower. At the same time, the U.S. dollar posted its worst calendar year since 2017, with the DXY down 9.5%, including a 4.6% decline against the Canadian dollar and a 12% depreciation against the euro*. Together, these dynamics provided a powerful tailwind for gold.

Additional support came from elevated geopolitical uncertainty, initially sparked by Russia’s invasion of Ukraine, compounded by conflicts in the Middle East, and most recently the capture of Venezuelan leader Nicolás Maduro, protests in Iran and threats against Greenland. In an environment shaped by sanctions, trade wars, and a push toward deglobalization, gold has served as a safe-haven asset against tail risks. Some central banks have also accelerated diversification away from a U.S. dollar-centric system, stepping up gold purchases over the past three years, reinforcing demand.

The graph shows that the dollar declined against the CAD and euro in 2025 helping boost gold prices.

The graph shows that the dollar declined against the CAD and euro in 2025 helping boost gold prices.

Tactical lens: Is gold overextended?

Gold's move in 2025 was historic, marking the fourth strongest annual return since the end of the Bretton Woods system in 1971, which suspended the U.S. dollar convertibility into gold*. But the question now is what happens next. To explore this, we look at (1) lessons from history and (2) what current macro conditions imply.

1) Lessons from history

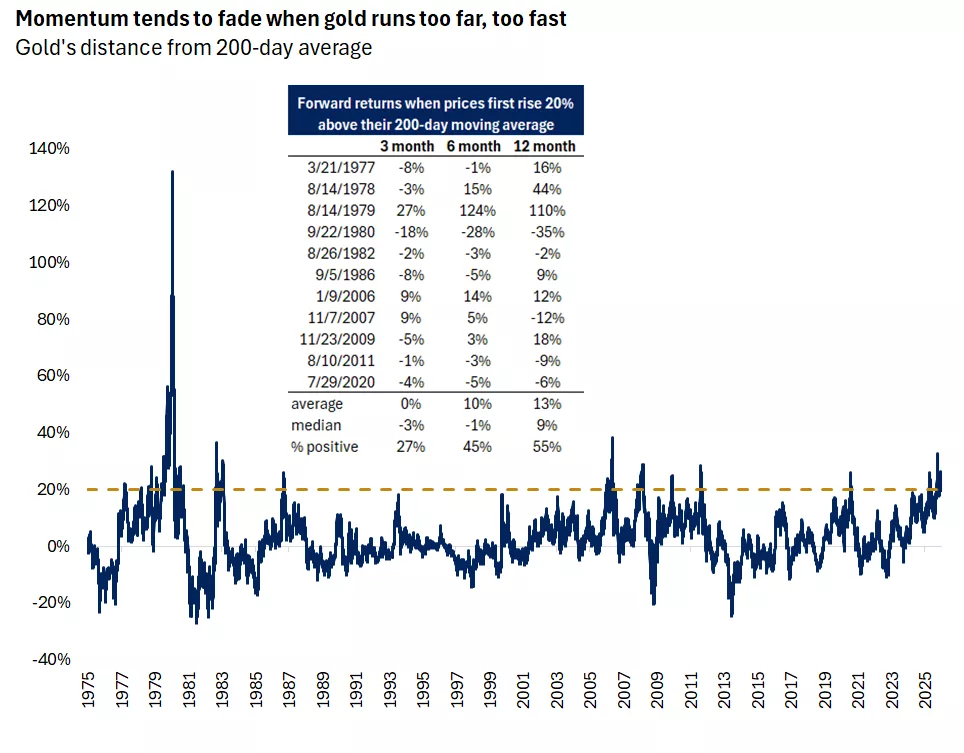

There have been 11 historical instances where gold surged 20% above its 200-day moving average, a sign of extreme momentum*. Forward returns after such strength have been mixed at best, with many periods showing muted or negative performance. Outside of a few standout winners (1978, 1979), upside momentum often fades*. However, crashes are rare. Historically, buying gold at extremes tends to lead to cooling, consolidation, or mild corrections. Flat-to-slightly negative returns have been the norm*.

2) Macro backdrop for 2026

Last year, global trade uncertainty and tariff headwinds dominated headlines, yet growth proved resilient. For 2026, we expect steady economic growth, slightly looser Fed policy alongside a BoC and ECB pause, modest fiscal stimulus tied to Canada's 2025 budget which includes investments in housing, infrastructure and defense, and possibly fading tariff uncertainty. Solid growth and lingering inflation pressures in the U.S. should prevent aggressive Fed easing, and while geopolitics remains a wild card, an oversupplied oil market reduces the risk of energy price spikes*. We also don’t anticipate another sharp U.S. dollar decline, though a modest softening is likely. Taken together, these conditions could keep gold rangebound, with a risk of correction if growth surprises to the upside, long-term yields fail to decline further and geopolitical risks subside.

Bottom Line: After 2025’s parabolic move, we expect gold’s momentum to cool with history suggesting the potential for consolidation or a correction, though not collapse.

The graph shows that forward gold returns after prices rise 20% above their 200-day moving average. Historically, momentum tends to fade when gold runs too far, too fast.

The graph shows that forward gold returns after prices rise 20% above their 200-day moving average. Historically, momentum tends to fade when gold runs too far, too fast.

Strategic lens: A portfolio diversifier

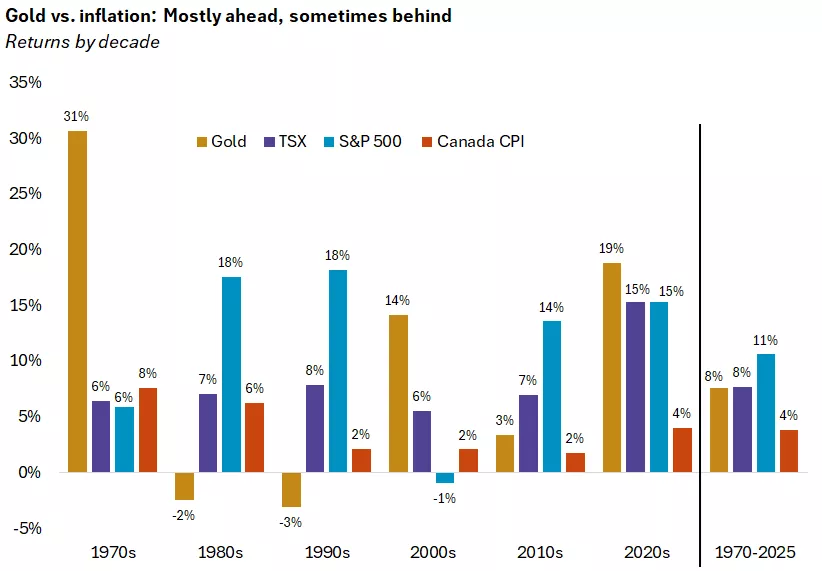

With prices potentially overextended, we believe investors should avoid chasing gold higher. Gold has had three standout periods of strong performance—the 1970s, the 2000s, and the past five years*. But over longer horizons, it has delivered higher volatility and lower returns than a global equity portfolio, often with extended stretches of sideways action and long recovery periods*. Once it peaked in 1980, it took until 1999 to make a new high). Since 1970, the TSX and S&P 500 have returned 8.5% and 11% annualized (including dividends) respectively versus 8% for gold*.

However, the case for gold is not about seeking above-average returns, but rather its diversification and stability benefits. Historically, gold has shown low correlation to both stocks and bonds (including the commodity-heavy TSX), meaning its returns tend to move independently of traditional assets*. This decoupling, especially during periods of market stress, makes gold a useful diversifier, helping smooth returns across cycles and improve portfolio efficiency.

From a fundamental perspective, gold has historically acted as a hedge against large, unexpected inflation spikes, when both stocks and bonds typically struggle. However, unlike a diversified stock portfolio, it offers limited protection against smaller or gradual price increases. This helps explain why it lagged inflation during the 1980s and 1990s, and only roughly kept pace with inflation during the 2010s. Gold has also tended to provide some protection during severe geopolitical, economic, or financial shocks (e.g., 2008)*.

Bottom line: While stocks have more consistently protected an investor's purchasing power over time, gold can serve as a strategic hedge against extreme uncertainty and help smooth volatility, complementing stocks and bonds in a diversified portfolio. Although our target allocation for commodities, which includes gold, remains 0%, for investors seeking to enhance diversification with precious metals or mitigate equity market volatility amid heightened fiscal, inflationary, and geopolitical risks, we believe a gold allocation of up to approximately 5% may be appropriate within the more aggressive portion of a well-diversified portfolio.

The graph shows returns for gold, stocks and inflation by decade. While gold has outpaced inflation over time that was not the case in the 1960s, 1980s and 1990s.

The graph shows returns for gold, stocks and inflation by decade. While gold has outpaced inflation over time that was not the case in the 1960s, 1980s and 1990s.

Additional considerations:

- If the goal is diversification and crisis protection, we think investors consider funding the gold allocation from equities.

- If the goal is inflation protection (against large, unexpected spikes), investors may consider reallocating from bonds.

- An equity-and-bond portfolio can still provide meaningful inflation protection and diversification without precious metals. Canada’s materials sector in the TSX—which we currently recommend overweighting relative to a benchmark allocation—already provides exposure to movements in precious metals. However, for those seeking an additional layer of crisis resilience and inflation hedging, gold can be a small complementary allocation.

Angelo Kourkafas, CFA;

Senior Global Investment Strategist

Important information:

Sources: * Bloomberg, Edward Jones

Investors should understand the risk of owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal. Diversification does not ensure a profit or protect against loss in a declining market.

This report is intended as educational only and should not be interpreted as specific recommendations or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.